More on Leadership

Alexander Nguyen

3 years ago

A Comparison of Amazon, Microsoft, and Google's Compensation

Learn or earn

In 2020, I started software engineering. My base wage has progressed as follows:

Amazon (2020): $112,000

Microsoft (2021): $123,000

Google (2022): $169,000

I didn't major in math, but those jumps appear more than a 7% wage increase. Here's a deeper look at the three.

The Three Categories of Compensation

Most software engineering compensation packages at IT organizations follow this format.

Minimum Salary

Base salary is pre-tax income. Most organizations give a base pay. This is paid biweekly, twice monthly, or monthly.

Recruiting Bonus

Sign-On incentives are one-time rewards to new hires. Companies need an incentive to switch. If you leave early, you must pay back the whole cost or a pro-rated amount.

Equity

Equity is complex and requires its own post. A company will promise to give you a certain amount of company stock but when you get it depends on your offer. 25% per year for 4 years, then it's gone.

If a company gives you $100,000 and distributes 25% every year for 4 years, expect $25,000 worth of company stock in your stock brokerage on your 1 year work anniversary.

Performance Bonus

Tech offers may include yearly performance bonuses. Depends on performance and funding. I've only seen 0-20%.

Engineers' overall compensation usually includes:

Base Salary + Sign-On + (Total Equity)/4 + Average Performance Bonus

Amazon: (TC: 150k)

Base Pay System

Amazon pays Seattle employees monthly on the first work day. I'd rather have my money sooner than later, even if it saves processing and pay statements.

The company upped its base pay cap from $160,000 to $350,000 to compete with other tech companies.

Performance Bonus

Amazon has no performance bonus, so you can work as little or as much as you like and get paid the same. Amazon is savvy to avoid promising benefits it can't deliver.

Sign-On Bonus

Amazon gives two two-year sign-up bonuses. First-year workers could receive $20,000 and second-year workers $15,000. It's probably to make up for the company's strange equity structure.

If you leave during the first year, you'll owe the entire money and a prorated amount for the second year bonus.

Equity

Most organizations prefer a 25%, 25%, 25%, 25% equity structure. Amazon takes a different approach with end-heavy equity:

the first year, 5%

15% after one year.

20% then every six months

We thought it was constructed this way to keep staff longer.

Microsoft (TC: 185k)

Base Pay System

Microsoft paid biweekly.

Gainful Performance

My offer letter suggested a 0%-20% performance bonus. Everyone will be satisfied with a 10% raise at year's end.

But misleading press where the budget for the bonus is doubled can upset some employees because they won't earn double their expected bonus. Still barely 10% for 2022 average.

Sign-On Bonus

Microsoft's sign-on bonus is a one-time payout. The contract can require 2-year employment. You must negotiate 1 year. It's pro-rated, so that's fair.

Equity

Microsoft is one of those companies that has standard 25% equity structure. Except if you’re a new graduate.

In that case it’ll be

25% six months later

25% each year following that

New grads will acquire equity in 3.5 years, not 4. I'm guessing it's to keep new grads around longer.

Google (TC: 300k)

Base Pay Structure

Google pays biweekly.

Performance Bonus

Google's offer letter specifies a 15% bonus. It's wonderful there's no cap, but I might still get 0%. A little more than Microsoft’s 10% and a lot more than Amazon’s 0%.

Sign-On Bonus

Google gave a 1-year sign-up incentive. If the contract is only 1 year, I can move without any extra obligations.

Not as fantastic as Amazon's sign-up bonuses, but the remainder of the package might compensate.

Equity

We covered Amazon's tail-heavy compensation structure, so Google's front-heavy equity structure may surprise you.

Annual structure breakdown

33% Year 1

33% Year 2

22% Year 3

12% Year 4

The goal is to get them to Google and keep them there.

Final Thoughts

This post hopefully helped you understand the 3 firms' compensation arrangements.

There's always more to discuss, such as refreshers, 401k benefits, and business discounts, but I hope this shows a distinction between these 3 firms.

KonstantinDr

3 years ago

Early Adopters And the Fifth Reason WHY

Product management wizardry.

Early adopters buy a product even if it hasn't hit the market or has flaws.

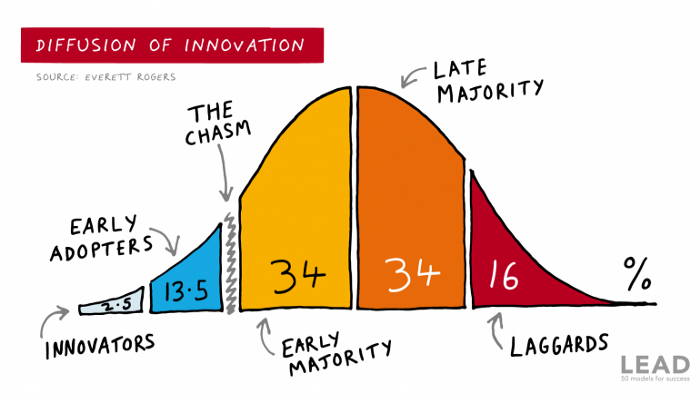

Who are the early adopters?

Early adopters try a new technology or product first. Early adopters are interested in trying or buying new technologies and products before others. They're risk-tolerant and can provide initial cash flow and product reviews. They help a company's new product or technology gain social proof.

Early adopters are most common in the technology industry, but they're in every industry. They don't follow the crowd. They seek innovation and report product flaws before mass production. If the product works well, the first users become loyal customers, and colleagues value their opinion.

What to do with early adopters?

They can be used to collect feedback and initial product promotion, first sales, and product value validation.

How to find early followers?

Start with your immediate environment and target audience. Communicate with them to see if they're interested in your value proposition.

1) Innovators (2.5% of the population) are risk-takers seeking novelty. These people are the first to buy new and trendy items and drive social innovation. However, these people are usually elite;

Early adopters (13.5%) are inclined to accept innovations but are more cautious than innovators; they start using novelties when innovators or famous people do;

3) The early majority (34%) is conservative; they start using new products when many people have mastered them. When the early majority accepted the innovation, it became ingrained in people's minds.

4) Attracting 34% of the population later means the novelty has become a mass-market product. Innovators are using newer products;

5) Laggards (16%) are the most conservative, usually elderly people who use the same products.

Stages of new information acceptance

1. The information is strange and rejected by most. Accepted only by innovators;

2. When early adopters join, more people believe it's not so bad; when a critical mass is reached, the novelty becomes fashionable and most people use it.

3. Fascination with a novelty peaks, then declines; the majority and laggards start using it later; novelty becomes obsolete; innovators master something new.

Problems with early implementation

Early adopter sales have disadvantages.

Higher risk of defects

Selling to first-time users increases the risk of defects. Early adopters are often influential, so this can affect the brand's and its products' long-term perception.

Not what was expected

First-time buyers may be disappointed by the product. Marketing messages can mislead consumers, and if the first users believe the company misrepresented the product, this will affect future sales.

Compatibility issues

Some technological advances cause compatibility issues. Consumers may be disappointed if new technology is incompatible with their electronics.

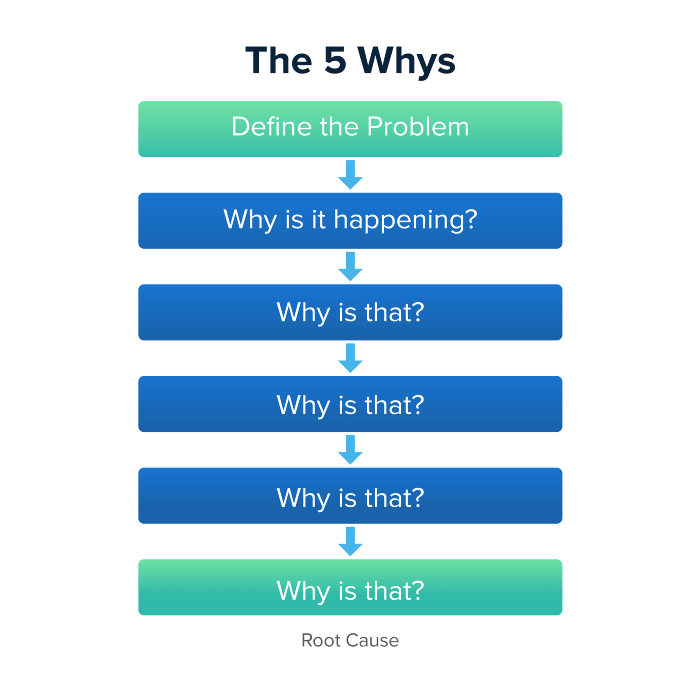

Method 5 WHY

Let's talk about 5 why, a good tool for finding project problems' root causes. This method is also known as the five why rule, method, or questions.

The 5 why technique came from Toyota's lean manufacturing and helps quickly determine a problem's root cause.

On one, two, and three, you simply do this:

We identify and frame the issue for which a solution is sought.

We frequently ponder this question. The first 2-3 responses are frequently very dull, making you want to give up on this pointless exercise. However, after that, things get interesting. And occasionally it's so fascinating that you question whether you really needed to know.

We consider the final response, ponder it, and choose a course of action.

Always do the 5 whys with the customer or team to have a reasonable discussion and better understand what's happening.

And the “five whys” is a wonderful and simplest tool for introspection. With the accumulated practice, it is used almost automatically in any situation like “I can’t force myself to work, the mood is bad in the morning” or “why did I decide that I have no life without this food processor for 20,000 rubles, which will take half of my rather big kitchen.”

An illustration of the five whys

A simple, but real example from my work practice that I think is very indicative, given the participants' low IT skills. Anonymized, of course.

Users spend too long looking for tender documents.

Why? Because they must search through many company tender documents.

Why? Because the system can't filter department-specific bids.

Why? Because our contract management system requirements didn't include a department-tender link. That's it, right? We'll add a filter and be happy. but still…

why? Because we based the system's requirements on regulations for working with paper tender documents (when they still had envelopes and autopsies), not electronic ones, and there was no search mechanism.

Why? We didn't consider how our work would change when switching from paper to electronic tenders when drafting the requirements.

Now I know what to do in the future. We add a filter, enter department data, and teach users to use it. This is tactical, but strategically we review the same forgotten requirements to make all the necessary changes in a package, plus we include it in the checklist for the acceptance of final requirements for the future.

Errors when using 5 why

Five whys seems simple, but it can be misused.

Popular ones:

The accusation of everyone and everything is then introduced. After all, the 5 why method focuses on identifying the underlying causes rather than criticizing others. As a result, at the third step, it is not a good idea to conclude that the system is ineffective because users are stupid and that we can therefore do nothing about it.

to fight with all my might so that the outcome would be exactly 5 reasons, neither more nor less. 5 questions is a typical number (it sounds nice, yes), but there could be 3 or 7 in actuality.

Do not capture in-between responses. It is difficult to overestimate the power of the written or printed word, so the result is so-so when the focus is lost. That's it, I suppose. Simple, quick, and brilliant, like other project management tools.

Conclusion

Today we analyzed important study elements:

Early adopters and 5 WHY We've analyzed cases and live examples of how these methods help with product research and growth point identification. Next, consider the HADI cycle.

Bart Krawczyk

2 years ago

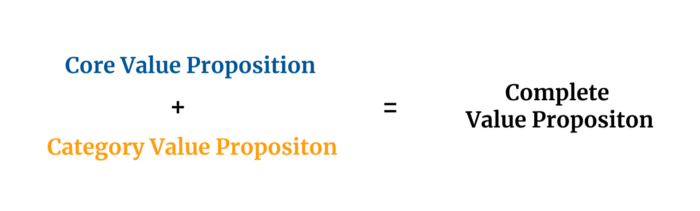

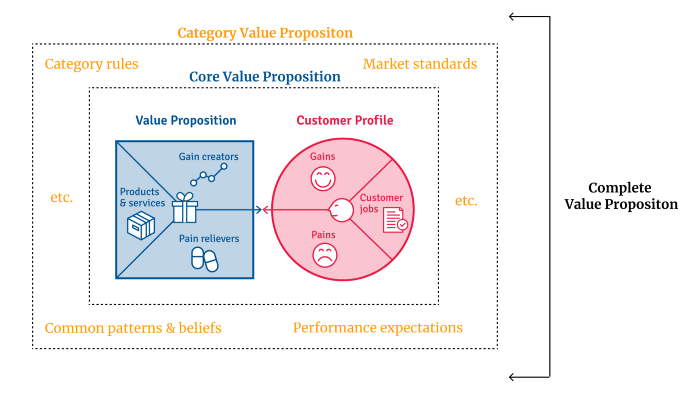

Understanding several Value Proposition kinds will help you create better goods.

Fixing problems isn't enough.

Numerous articles and how-to guides on value propositions focus on fixing consumer concerns.

Contrary to popular opinion, addressing customer pain rarely suffices. Win your market category too.

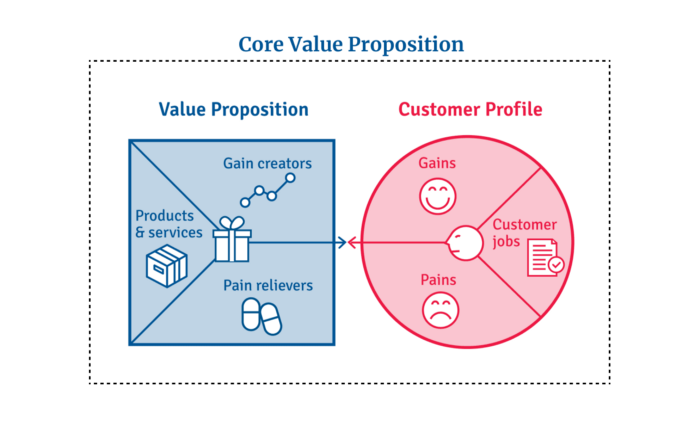

Core Value Statement

Value proposition usually means a product's main value.

Its how your product solves client problems. The product's core.

Answering these questions creates a relevant core value proposition:

What tasks is your customer trying to complete? (Jobs for clients)

How much discomfort do they feel while they perform this? (pains)

What would they like to see improved or changed? (gains)

After that, you create products and services that alleviate those pains and give value to clients.

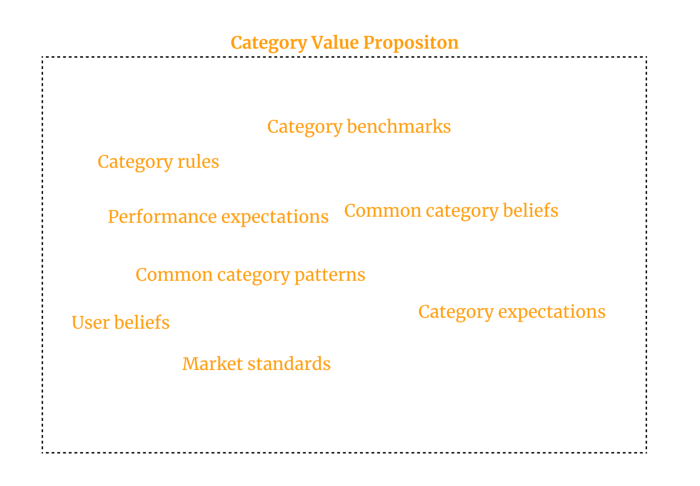

Value Proposition by Category

Your product belongs to a market category and must follow its regulations, regardless of its value proposition.

Creating a new market category is challenging. Fitting into customers' product perceptions is usually better than trying to change them.

New product users simplify market categories. Products are labeled.

Your product will likely be associated with a collection of products people already use.

Example: IT experts will use your communication and management app.

If your target clients think it's an advanced mail software, they'll compare it to others and expect things like:

comprehensive calendar

spam detectors

adequate storage space

list of contacts

etc.

If your target users view your product as a task management app, things change. You can survive without a contact list, but not status management.

Find out what your customers compare your product to and if it fits your value offer. If so, adapt your product plan to dominate this market. If not, try different value propositions and messaging to put the product in the right context.

Finished Value Proposition

A comprehensive value proposition is when your solution addresses user problems and wins its market category.

Addressing simply the primary value proposition may produce a valuable and original product, but it may struggle to cross the chasm into the mainstream market. Meeting expectations is easier than changing views.

Without a unique value proposition, you will drown in the red sea of competition.

To conclude:

Find out who your target consumer is and what their demands and problems are.

To meet these needs, develop and test a primary value proposition.

Speak with your most devoted customers. Recognize the alternatives they use to compare you against and the market segment they place you in.

Recognize the requirements and expectations of the market category.

To meet or surpass category standards, modify your goods.

Great products solve client problems and win their category.

You might also like

Jon Brosio

3 years ago

Every time I use this 6-part email sequence, I almost always make four figures.

(And you can have it for free)

Master email to sell anything.

Most novice creators don't know how to begin.

Many use online templates. These are usually fluff-filled and niche-specific.

They're robotic and "salesy."

I've attended 3 courses, read 10 books, and sent 600,000 emails in the past five years.

Outcome?

This *proven* email sequence assures me a month's salary every time I send it.

What you will discover in this article is that:

A full 6-part email sales cycle

The essential elements you must incorporate

placeholders and text-filled images

(Applies to any niche)

This can be a product introduction, holiday, or welcome sequence. This works for email-saleable products.

Let's start

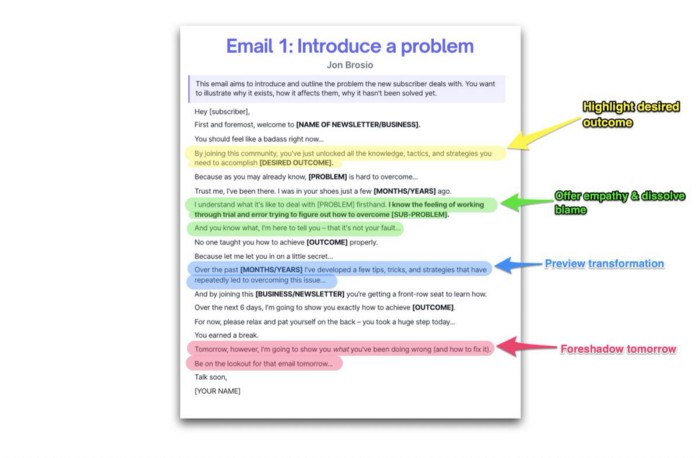

Email 1: Describe your issue

This email is crucial.

How to? We introduce a subscriber or prospect's problem. Later, we'll frame our offer as the solution.

Label the:

Problem

Why it still hasn't been fixed

Resulting implications for the customer

This puts our new subscriber in solve mode and queues our offer:

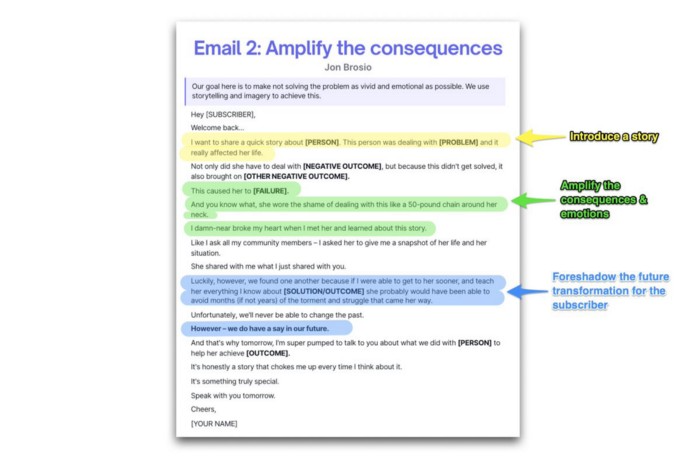

Email 2: Amplify the consequences

We're still causing problems.

We've created the problem, but now we must employ emotion and storytelling to make it real. We also want to forecast life if nothing changes.

Let's feel:

What occurs if it is not resolved?

Why is it crucial to fix it immediately?

Tell a tale of a person who was in their position. To emphasize the effects, use a true account of another person (or of yourself):

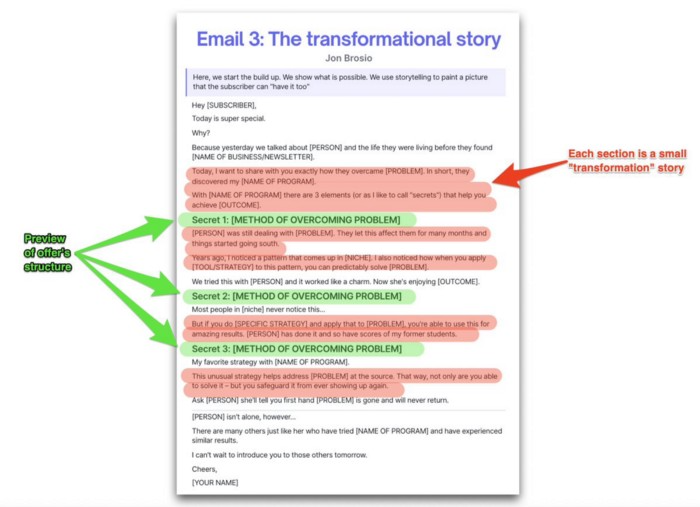

Email 3: Share a transformation story

Selling stories.

Whether in an email, landing page, article, or video. Humanize stories. They give information meaning.

This is where "issue" becomes "solution."

Let's reveal:

A tale of success

A new existence and result

tools and tactics employed

Start by transforming yourself.

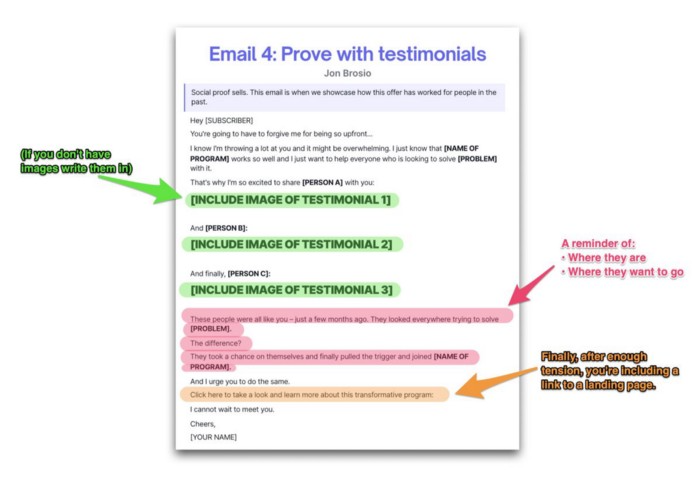

Email 4: Prove with testimonials

No one buys what you say.

Emotionally stirred people buy and act. They believe in the product. They feel that if they buy, it will work.

Social proof shows prospects that your solution will help them.

Add:

Earlier and Later

Testimonials

Reviews

Proof this deal works:

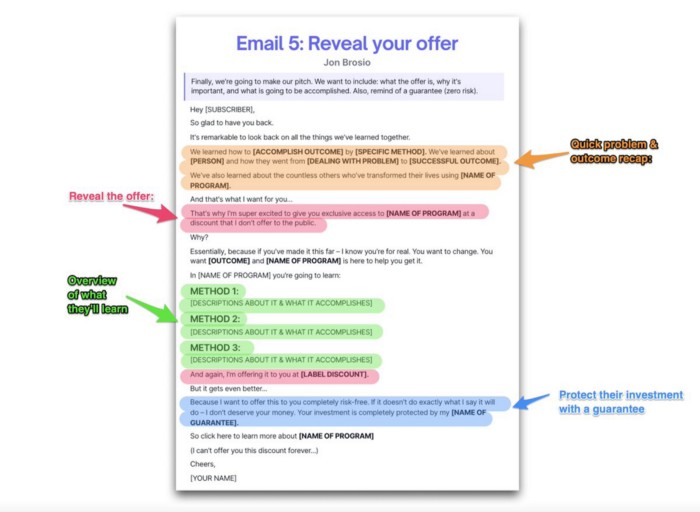

Email 5: Reveal your offer

It's showtime.

This is it. Until now, describing the offer and offering links to a landing page have been sparse in the email pictures.

We've been tense. Gaining steam. Building suspense. Email 5 reveals all.

In this email:

a description of the deal

A word about a promise

recapitulation of the transformation

and make a reference to the urgency Everything should be spelled out clearly:

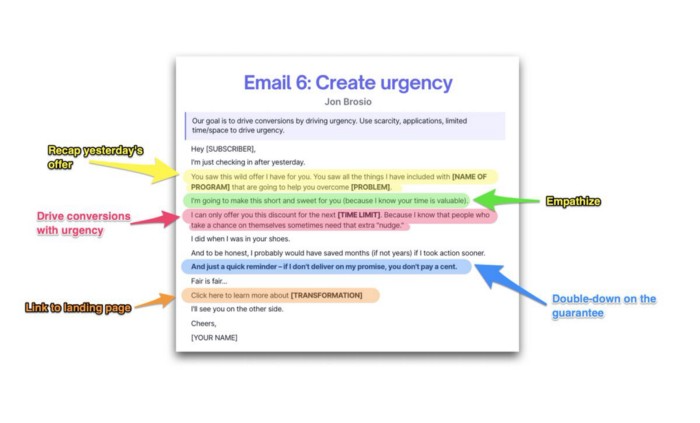

Email no. 6: Instill urgency

When there are stakes, humans act.

Creating and marketing with haste raises the stakes. Urgency makes a prospect act because they'll miss out or gain immensely.

Urgency converts. Use:

short time

Screening

Scarcity

Urgency and conversions. Limited-time offers are easy.

TL;DR

Use this proven 6-part email sequence (that turns subscribers into profit):

Introduce a problem

Amplify it with emotions

Share transformation story

Prove it works with testimonials

Value-stack and present your offer

Drive urgency and entice the purchase

Scott Galloway

3 years ago

Don't underestimate the foolish

ZERO GRACE/ZERO MALICE

Big companies and wealthy people make stupid mistakes too.

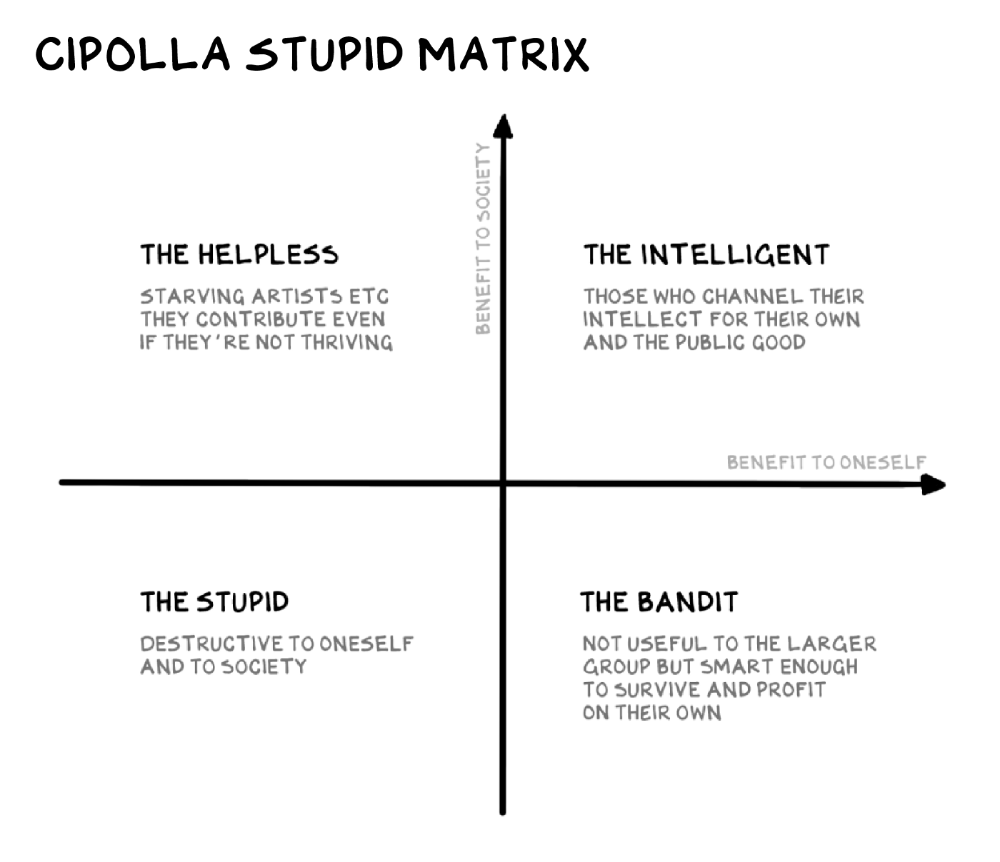

Your ancestors kept snakes and drank bad water. You (probably) don't because you've learnt from their failures via instinct+, the ultimate life-lessons streaming network in your head. Instincts foretell the future. If you approach a lion, it'll eat you. Our society's nuanced/complex decisions have surpassed instinct. Human growth depends on how we handle these issues. 80% of people believe they are above-average drivers, yet few believe they make many incorrect mistakes that make them risky. Stupidity hurts others like death. Basic Laws of Human Stupidity by Carlo Cipollas:

Everyone underestimates the prevalence of idiots in our society.

Any other trait a person may have has no bearing on how likely they are to be stupid.

A dumb individual is one who harms someone without benefiting themselves and may even lose money in the process.

Non-dumb people frequently underestimate how destructively powerful stupid people can be.

The most dangerous kind of person is a moron.

Professor Cippola defines stupid as bad for you and others. We underestimate the corporate world's and seemingly successful people's ability to make bad judgments that harm themselves and others. Success is an intoxication that makes you risk-aggressive and blurs your peripheral vision.

Stupid companies and decisions:

Big Dumber

Big-company bad ideas have more bulk and inertia. The world's most valuable company recently showed its board a VR headset. Jony Ive couldn't destroy Apple's terrible idea in 2015. Mr. Ive said that VR cut users off from the outer world, made them seem outdated, and lacked practical uses. Ives' design team doubted users would wear headsets for lengthy periods.

VR has cost tens of billions of dollars over a decade to prove nobody wants it. The next great SaaS startup will likely come from Florence, not Redmond or San Jose.

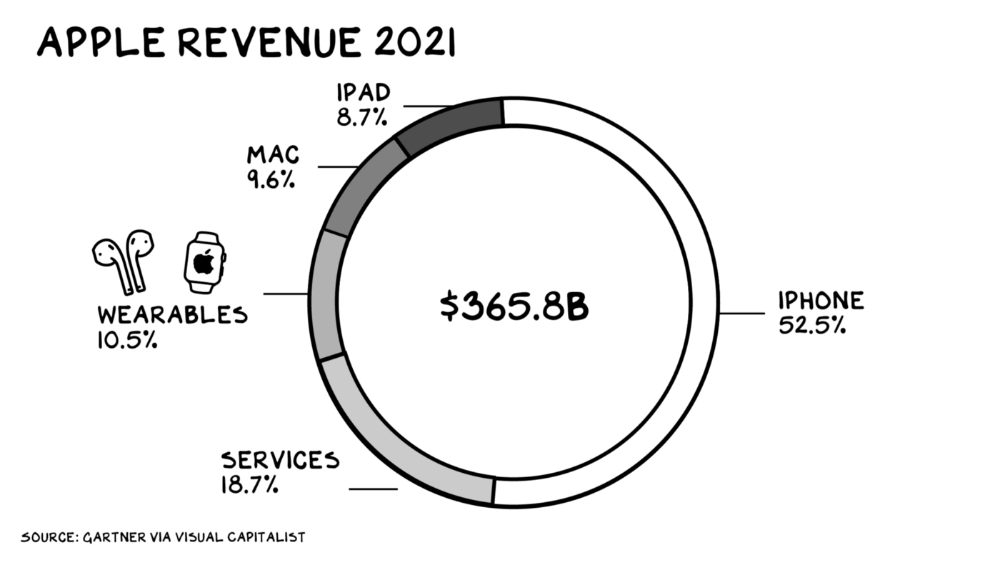

Apple Watch and Airpods have made the Cupertino company the world's largest jewelry maker. 10.5% of Apple's income, or $38 billion, comes from wearables in 2021. (seven times the revenue of Tiffany & Co.). Jewelry makes you more appealing and useful. Airpods and Apple Watch do both.

Headsets make you less beautiful and useful and promote isolation, loneliness, and unhappiness among American teenagers. My sons pretend they can't hear or see me when on their phones. VR headsets lack charisma.

Coinbase disclosed a plan to generate division and tension within its workplace weeks after Apple was pitched $2,000 smokes. The crypto-trading platform is piloting a program that rates staff after every interaction. If a coworker says anything you don't like, you should tell them how to improve. Everyone gets a 110-point scorecard. Coworkers should evaluate a person's rating while deciding whether to listen to them. It's ridiculous.

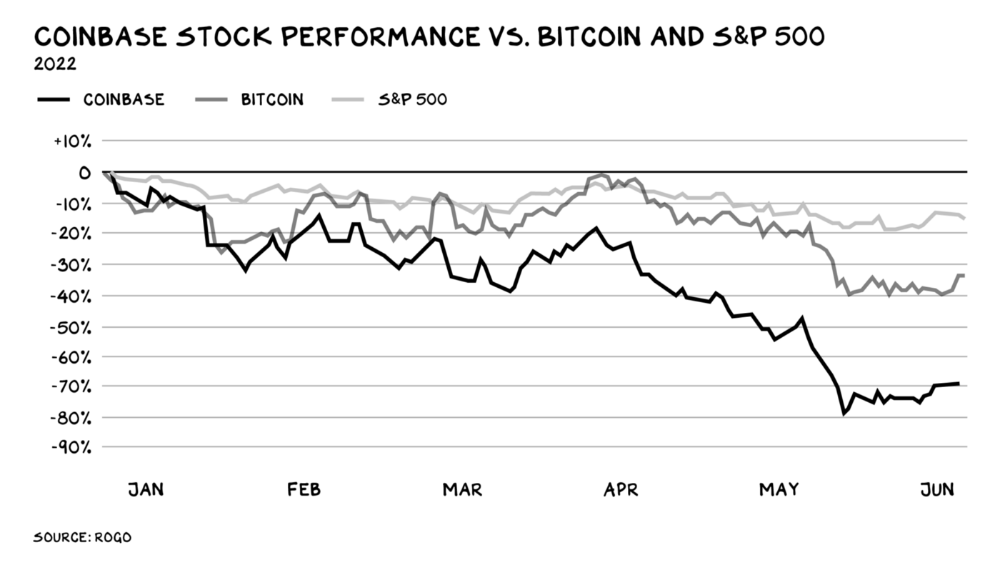

Organizations leverage our superpower of cooperation. This encourages non-cooperation, period. Bridgewater's founder Ray Dalio designed the approach to promote extreme transparency. Dalio has 223 billion reasons his managerial style works. There's reason to suppose only a small group of people, largely traders, will endure a granular scorecard. Bridgewater has 20% first-year turnover. Employees cry in bathrooms, and sex scandals are settled by ignoring individuals with poor believability levels. Coinbase might take solace that the stock is 80% below its initial offering price.

Poor Stupid

Fools' ledgers are valuable. More valuable are lists of foolish rich individuals.

Robinhood built a $8 billion corporation on financial ignorance. The firm's median account value is $240, and its stock has dropped 75% since last summer. Investors, customers, and society lose. Stupid. Luna published a comparable list on the blockchain, grew to $41 billion in market cap, then plummeted.

A podcast presenter is recruiting dentists and small-business owners to invest in Elon Musk's Twitter takeover. Investors pay a 7% fee and 10% of the upside for the chance to buy Twitter at a 35% premium to the current price. The proposal legitimizes CNBC's Trade Like Chuck advertising (Chuck made $4,600 into $460,000 in two years). This is stupid because it adds to the Twitter deal's desperation. Mr. Musk made an impression when he urged his lawyers to develop a legal rip-cord (There are bots on the platform!) to abandon the share purchase arrangement (for less than they are being marketed by the podcaster). Rolls-Royce may pay for this list of the dumb affluent because it includes potential Cullinan buyers.

Worst company? Flowcarbon, founded by WeWork founder Adam Neumann, operates at the convergence of carbon and crypto to democratize access to offsets and safeguard the earth's natural carbon sinks. Can I get an ayahuasca Big Gulp?

Neumann raised $70 million with their yogababble drink. More than half of the consideration came from selling GNT. Goddess Nature Token. I hope the company gets an S-1. Or I'll start a decentralized AI Meta Renewable NFTs company. My Community Based Ebitda coin will fund the company. Possible.

Stupidity inside oneself

This weekend, I was in NYC with my boys. My 14-year-old disappeared. He's realized I'm not cool and is mad I let the charade continue. When out with his dad, he likes to stroll home alone and depart before me. Friends told me hell would return, but I was surprised by how fast the eye roll came.

Not so with my 11-year-old. We went to The Edge, a Hudson Yards observation platform where you can see the city from 100 storeys up for $38. This is hell's seventh ring. Leaning into your boys' interests is key to engaging them (dad tip). Neither loves Crossfit, WW2 history, or antitrust law.

We take selfies on the Thrilling Glass Floor he spots. Dad, there's a bar! Coke? I nod, he rushes to the bar, stops, runs back for money, and sprints back. Sitting on stone seats, drinking Atlanta Champagne, he turns at me and asks, Isn't this amazing? I'll never reach paradise.

Later that night, the lads are asleep and I've had two Zacapas and Cokes. I SMS some friends about my day and how I feel about sons/fatherhood/etc. How I did. They responded and approached. The next morning, I'm sober, have distance from my son, and feel ashamed by my texts. Less likely to impulsively share my emotions with others. Stupid again.

INTΞGRITY team

3 years ago

Privacy Policy

Effective date: August 31, 2022

This Privacy Statement describes how INTΞGRITY ("we," or "us") collects, uses, and discloses your personal information. This Privacy Statement applies when you use our websites, mobile applications, and other online products and services that link to this Privacy Statement (collectively, our "Services"), communicate with our customer care team, interact with us on social media, or otherwise interact with us.

This Privacy Policy may be modified from time to time. If we make modifications, we will update the date at the top of this policy and, in certain instances, we may give you extra notice (such as adding a statement to our website or providing you with a notification). We encourage you to routinely review this Privacy Statement to remain informed about our information practices and available options.

INFORMATION COLLECTION

The Data You Provide to Us

We collect information that you directly supply to us. When you register an account, fill out a form, submit or post material through our Services, contact us via third-party platforms, request customer assistance, or otherwise communicate with us, you provide us with information directly. We may collect your name, display name, username, bio, email address, company information, your published content, including your avatar image, photos, posts, responses, and any other information you voluntarily give.

In certain instances, we may collect the information you submit about third parties. We will use your information to fulfill your request and will not send emails to your contacts unrelated to your request unless they separately opt to receive such communications or connect with us in some other way.

We do not collect payment details via the Services.

Automatically Collected Information When You Communicate with Us

In certain cases, we automatically collect the following information:

We gather data regarding your behavior on our Services, such as your reading history and when you share links, follow users, highlight posts, and like posts.

Device and Usage Information: We gather information about the device and network you use to access our Services, such as your hardware model, operating system version, mobile network, IP address, unique device identifiers, browser type, and app version. We also collect information regarding your activities on our Services, including access times, pages viewed, links clicked, and the page you visited immediately prior to accessing our Services.

Information Obtained Through Cookies and Comparable Tracking Technologies: We collect information about you through tracking technologies including cookies and web beacons. Cookies are little data files kept on your computer's hard disk or device's memory that assist us in enhancing our Services and your experience, determining which areas and features of our Services are the most popular, and tracking the number of visitors. Web beacons (also known as "pixel tags" or "clear GIFs") are electronic pictures that we employ on our Services and in our communications to assist with cookie delivery, session tracking, and usage analysis. We also partner with third-party analytics providers who use cookies, web beacons, device identifiers, and other technologies to collect information regarding your use of our Services and other websites and applications, including your IP address, web browser, mobile network information, pages viewed, time spent on pages or in mobile apps, and links clicked. INTΞGRITY and others may use your information to, among other things, analyze and track data, evaluate the popularity of certain content, present content tailored to your interests on our Services, and better comprehend your online activities. See Your Options for additional information on cookies and how to disable them.

Information Obtained from Outside Sources

We acquire information from external sources. We may collect information about you, for instance, through social networks, accounting service providers, and data analytics service providers. In addition, if you create or log into your INTΞGRITY account via a third-party platform (such as Apple, Facebook, Google, or Twitter), we will have access to certain information from that platform, including your name, lists of friends or followers, birthday, and profile picture, in accordance with the authorization procedures determined by that platform.

We may derive information about you or make assumptions based on the data we gather. We may deduce your location based on your IP address or your reading interests based on your reading history, for instance.

USAGE OF INFORMATION

We use the information we collect to deliver, maintain, and enhance our Services, including publishing and distributing user-generated content, and customizing the posts you see. Additionally, we utilize collected information to: create and administer your INTΞGRITY account;

Send transaction-related information, including confirmations, receipts, and user satisfaction surveys;

Send you technical notices, security alerts, and administrative and support messages;

Respond to your comments and queries and offer support;

Communicate with you about new INTΞGRITY content, goods, services, and features, as well as other news and information that we believe may be of interest to you (see Your Choices for details on how to opt out of these communications at any time);

Monitor and evaluate usage, trends, and activities associated with our Services;

Detect, investigate, and prevent security incidents and other harmful, misleading, fraudulent, or illegal conduct, and safeguard INTΞGRITY’s and others' rights and property;

Comply with our legal and financial requirements; and Carry out any other purpose specified to you at the time the information was obtained.

SHARING OF INFORMATION

We share personal information where required by law or as otherwise specified in this policy:

Personal information is shared with other Service users. If you use our Services to publish content, make comments, or send private messages, for instance, certain information about you, such as your name, photo, bio, and other account information you may supply, as well as information about your activity on our Services, will be available to others (e.g., your followers and who you follow, recent posts, likes, highlights, and responses).

We share personal information with vendors, service providers, and consultants who require access to such information to perform services on our behalf, such as companies that assist us with web hosting, storage, and other infrastructure, analytics, fraud prevention, and security, customer service, communications, and marketing.

We may release personally identifiable information if we think that doing so is in line with or required by any relevant law or legal process, including authorized demands from public authorities to meet national security or law enforcement obligations. If we intend to disclose your personal information in response to a court order, we will provide you with prior notice so that you may contest the disclosure (for example, by seeking court intervention), unless we are prohibited by law or believe that doing so could endanger others or lead to illegal conduct. We shall object to inappropriate legal requests for information regarding users of our Services.

If we believe your actions are inconsistent with our user agreements or policies, if we suspect you have violated the law, or if we believe it is necessary to defend the rights, property, and safety of INTΞGRITY, our users, the public, or others, we may disclose your personal information.

We share personal information with our attorneys and other professional advisers when necessary for obtaining counsel or otherwise protecting and managing our business interests.

We may disclose personal information in conjunction with or during talks for any merger, sale of corporate assets, financing, or purchase of all or part of our business by another firm.

Personal information is transferred between and among INTΞGRITY, its current and future parents, affiliates, subsidiaries, and other companies under common ownership and management.

We will only share your personal information with your permission or at your instruction.

We also disclose aggregated or anonymized data that cannot be used to identify you.

IMPLEMENTATIONS FROM THIRD PARTIES

Some of the content shown on our Services is not hosted by INTΞGRITY. Users are able to publish content hosted by a third party but embedded in our pages ("Embed"). When you interact with an Embed, it can send information to the hosting third party just as if you had visited the hosting third party's website directly. When you load an INTΞGRITY post page with a YouTube video Embed and view the video, for instance, YouTube collects information about your behavior, such as your IP address and how much of the video you watch. INTΞGRITY has no control over the information that third parties acquire via Embeds or what they do with it. This Privacy Statement does not apply to data gathered via Embeds. Before interacting with the Embed, it is recommended that you review the privacy policy of the third party hosting the Embed, which governs any information the Embed gathers.

INFORMATION TRANSFER TO THE UNITED STATES AND OTHER NATIONS

INTΞGRITY’s headquarters are located in the United States, and we have operations and service suppliers in other nations. Therefore, we and our service providers may transmit, store, or access your personal information in jurisdictions that may not provide a similar degree of data protection to your home jurisdiction. For instance, we transfer personal data to Amazon Web Services, one of our service providers that processes personal information on our behalf in numerous data centers throughout the world, including those indicated above. We shall take measures to guarantee that your personal information is adequately protected in the jurisdictions where it is processed.

YOUR SETTINGS

Account Specifics

You can access, modify, delete, and export your account information at any time by login into the Services and visiting the Settings page. Please be aware that if you delete your account, we may preserve certain information on you as needed by law or for our legitimate business purposes.

Cookies

The majority of web browsers accept cookies by default. You can often configure your browser to delete or refuse cookies if you wish. Please be aware that removing or rejecting cookies may impact the accessibility and performance of our services.

Communications

You may opt out of getting certain messages from us, such as digests, newsletters, and activity notifications, by following the instructions contained within those communications or by visiting the Settings page of your account. Even if you opt out, we may still send you emails regarding your account or our ongoing business relationships.

Mobile Push Notifications

We may send push notifications to your mobile device with your permission. You can cancel these messages at any time by modifying your mobile device's notification settings.

YOUR CALIFORNIA PRIVACY RIGHTS

The California Consumer Privacy Act, or "CCPA" (Cal. Civ. Code 1798.100 et seq. ), grants California residents some rights regarding their personal data. If you are a California resident, you are subject to this clause.

We have collected the following categories of personal information over the past year: identifiers, commercial information, internet or other electronic network activity information, and conclusions. Please refer to the section titled "Collection of Information" for specifics regarding the data points we gather and the sorts of sources from which we acquire them. We collect personal information for the business and marketing purposes outlined in the section on Use of Information. In the past 12 months, we have shared the following types of personal information to the following groups of recipients for business purposes:

Category of Personal Information: Identifiers

Categories of Recipients: Analytics Providers, Communication Providers, Custom Service Providers, Fraud Prevention and Security Providers, Infrastructure Providers, Marketing Providers, Payment Processors

Category of Personal Information: Commercial Information

Categories of Recipients: Analytics Providers, Infrastructure Providers, Payment Processors

Category of Personal Information: Internet or Other Electronic Network Activity Information

Categories of Recipients: Analytics Providers, Infrastructure Providers

Category of Personal Information: Inferences

Categories of Recipients: Analytics Providers, Infrastructure Providers

INTΞGRITY does not sell personally identifiable information.

You have the right, subject to certain limitations: (1) to request more information about the categories and specific pieces of personal information we collect, use, and disclose about you; (2) to request the deletion of your personal information; (3) to opt out of any future sales of your personal information; and (4) to not be discriminated against for exercising these rights. You may submit these requests by email to hello@int3grity.com. We shall not treat you differently if you exercise your rights under the CCPA.

If we receive your request from an authorized agent, we may request proof that you have granted the agent a valid power of attorney or that the agent otherwise possesses valid written authorization to submit requests on your behalf. This may involve requiring identity verification. Please contact us if you are an authorized agent wishing to make a request.

ADDITIONAL DISCLOSURES FOR INDIVIDUALS IN EUROPE

This section applies to you if you are based in the European Economic Area ("EEA"), the United Kingdom, or Switzerland and have specific rights and safeguards regarding the processing of your personal data under relevant law.

Legal Justification for Processing

We will process your personal information based on the following legal grounds:

To fulfill our obligations under our agreement with you (e.g., providing the products and services you requested).

When we have a legitimate interest in processing your personal information to operate our business or to safeguard our legitimate interests, we will do so (e.g., to provide, maintain, and improve our products and services, conduct data analytics, and communicate with you).

To meet our legal responsibilities (e.g., to maintain a record of your consents and track those who have opted out of non-administrative communications).

If we have your permission to do so (e.g., when you opt in to receive non-administrative communications from us). When consent is the legal basis for our processing of your personal information, you may at any time withdraw your consent.

Data Retention

We retain the personal information associated with your account so long as your account is active. If you close your account, your account information will be deleted within 14 days. We retain other personal data for as long as is required to fulfill the objectives for which it was obtained and for other legitimate business purposes, such as to meet our legal, regulatory, or other compliance responsibilities.

Data Access Requests

You have the right to request access to the personal data we hold on you and to get your data in a portable format, to request that your personal data be rectified or erased, and to object to or request that we restrict particular processing, subject to certain limitations. To assert your legal rights:

If you sign up for an INTΞGRITY account, you can request an export of your personal information at any time via the Settings website, or by visiting Settings and selecting Account from inside our app.

You can edit the information linked with your account on the Settings website, or by navigating to Settings and then Account in our app, and the Customize Your Interests page.

You may withdraw consent at any time by deleting your account via the Settings page, or by visiting Settings and then selecting Account within our app (except to the extent INTΞGRITY is prevented by law from deleting your information).

You may object to the use of your personal information at any time by contacting hello@int3grity.com.

Questions or Complaints

If we are unable to settle your concern over our processing of personal data, you have the right to file a complaint with the Data Protection Authority in your country. The links below provide access to the contact information for your Data Protection Authority.

For people in the EEA, please visit https://edpb.europa.eu/about-edpb/board/members en.

For persons in the United Kingdom, please visit https://ico.org.uk/global/contact-us.

For people in Switzerland: https://www.edoeb.admin.ch/edoeb/en/home/the-fdpic/contact.html

CONTACT US

Please contact us at hello@int3grity.com if you have any queries regarding this Privacy Statement.