More on Entrepreneurship/Creators

Navdeep Yadav

3 years ago

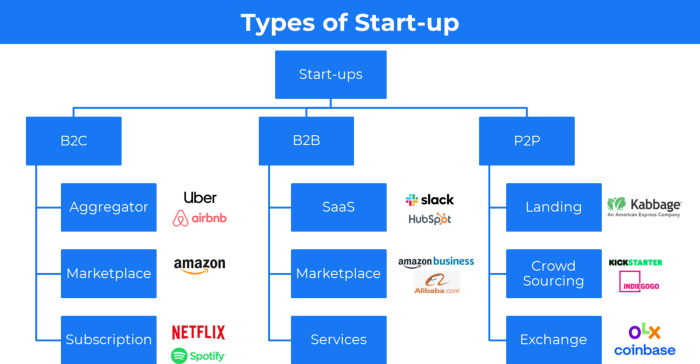

31 startup company models (with examples)

Many people find the internet's various business models bewildering.

This article summarizes 31 startup e-books.

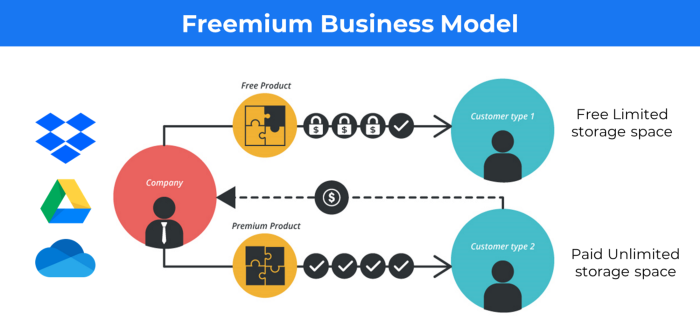

1. Using the freemium business model (free plus premium),

The freemium business model offers basic software, games, or services for free and charges for enhancements.

Examples include Slack, iCloud, and Google Drive

Provide a rudimentary, free version of your product or service to users.

Google Drive and Dropbox offer 15GB and 2GB of free space but charge for more.

Freemium business model details (Click here)

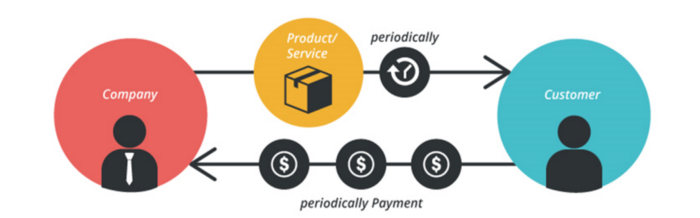

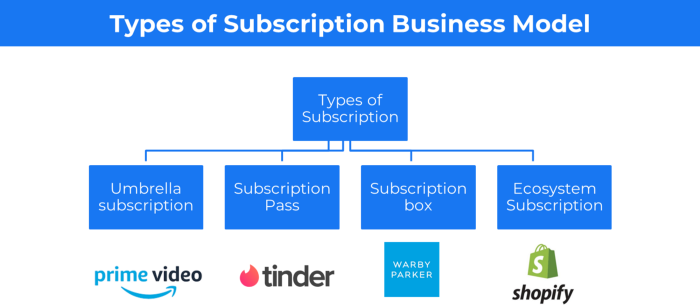

2. The Business Model of Subscription

Subscription business models sell a product or service for recurring monthly or yearly revenue.

Examples: Tinder, Netflix, Shopify, etc

It's the next step to Freemium if a customer wants to pay monthly for premium features.

Subscription Business Model (Click here)

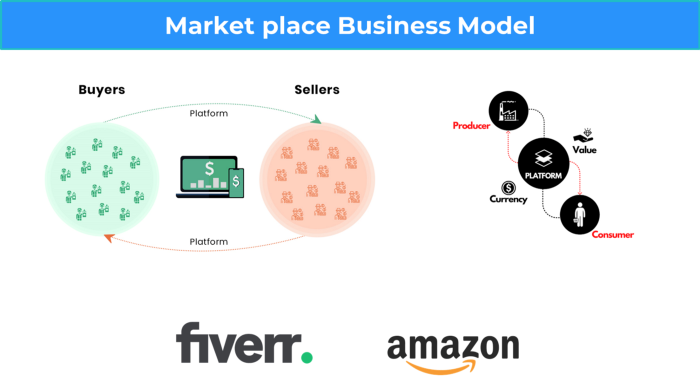

3. A market-based business strategy

It's an e-commerce site or app where third-party sellers sell products or services.

Examples are Amazon and Fiverr.

On Amazon's marketplace, a third-party vendor sells a product.

Freelancers on Fiverr offer specialized skills like graphic design.

Marketplace's business concept is explained.

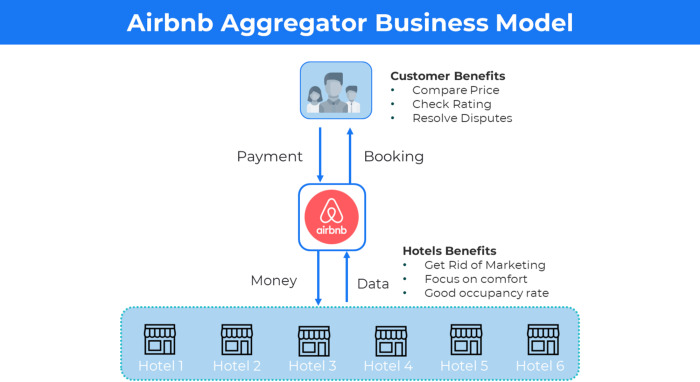

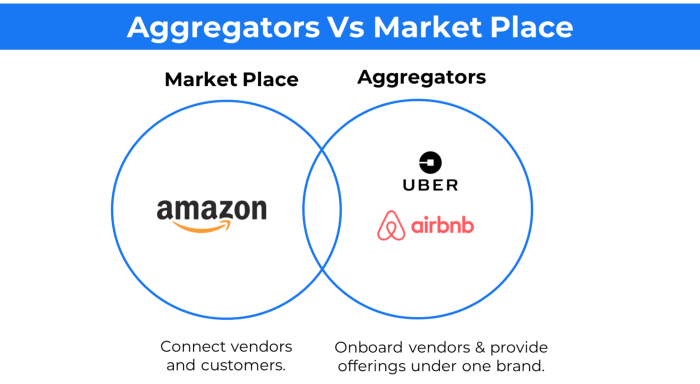

4. Business plans using aggregates

In the aggregator business model, the service is branded.

Uber, Airbnb, and other examples

Marketplace and Aggregator business models differ.

Amazon and Fiverr link merchants and customers and take a 10-20% revenue split.

Uber and Airbnb-style aggregator Join these businesses and provide their products.

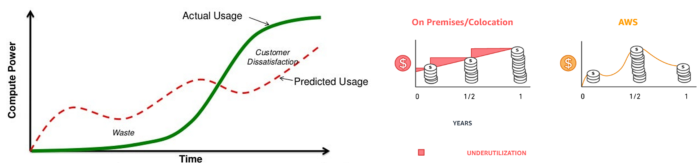

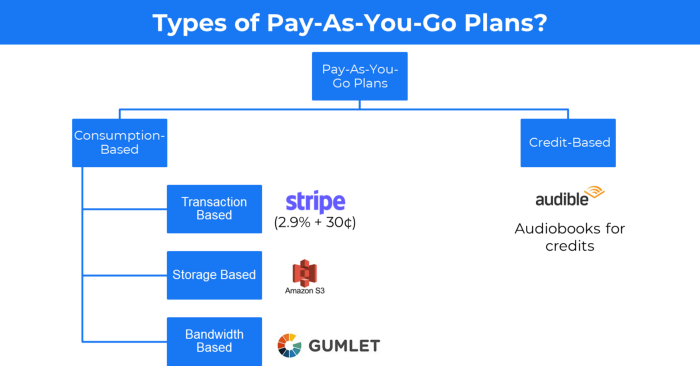

5. The pay-as-you-go concept of business

This is a consumption-based pricing system. Cloud companies use it.

Example: Amazon Web Service and Google Cloud Platform (GCP) (AWS)

AWS, an Amazon subsidiary, offers over 200 pay-as-you-go cloud services.

“In short, the more you use the more you pay”

When it's difficult to divide clients into pricing levels, pay-as-you is employed.

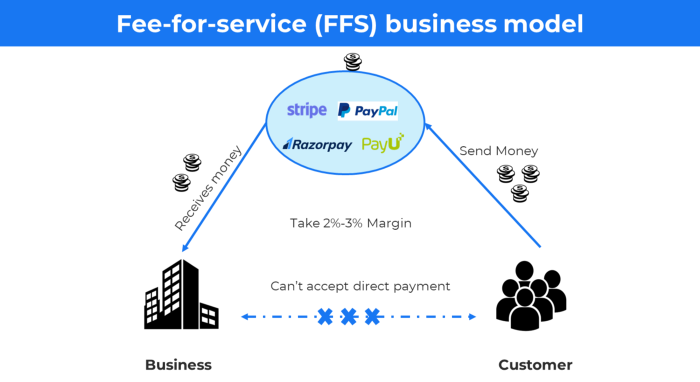

6. The business model known as fee-for-service (FFS)

FFS charges fixed and variable fees for each successful payment.

For instance, PayU, Paypal, and Stripe

Stripe charges 2.9% + 30 per payment.

These firms offer a payment gateway to take consumer payments and deposit them to a business account.

Fintech business model

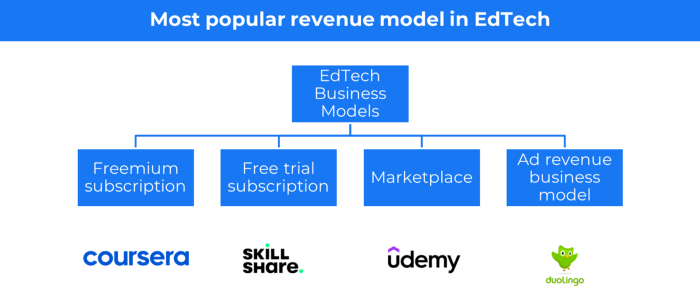

7. EdTech business strategy

In edtech, you generate money by selling material or teaching as a service.

edtech business models

Freemium When course content is free but certification isn't, e.g. Coursera

FREE TRIAL SkillShare offers free trials followed by monthly or annual subscriptions.

Self-serving marketplace approach where you pick what to learn.

Ad-revenue model The company makes money by showing adverts to its huge user base.

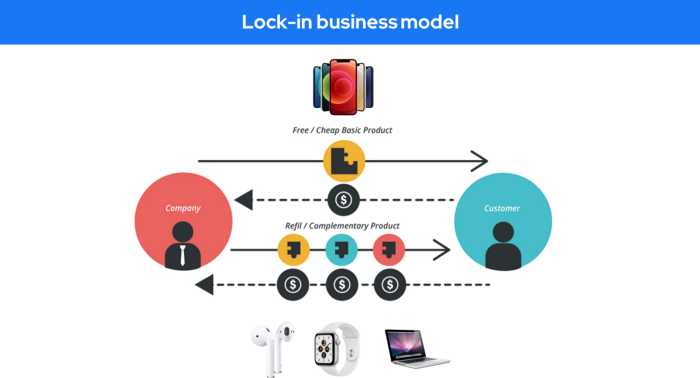

Lock-in business strategy

Lock in prevents customers from switching to a competitor's brand or offering.

It uses switching costs or effort to transmit (soft lock-in), improved brand experience, or incentives.

Apple, SAP, and other examples

Apple offers an iPhone and then locks you in with extra hardware (Watch, Airpod) and platform services (Apple Store, Apple Music, cloud, etc.).

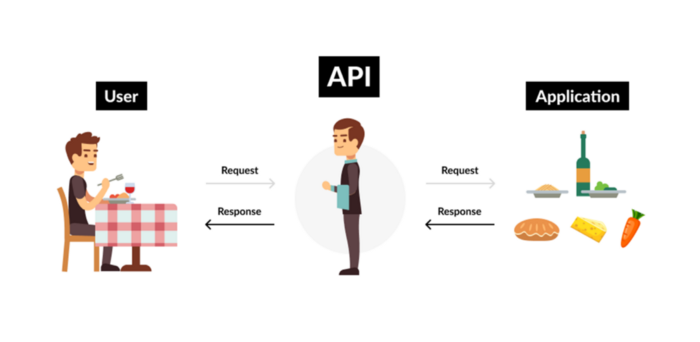

9. Business Model for API Licensing

APIs let third-party apps communicate with your service.

Uber and Airbnb use Google Maps APIs for app navigation.

Examples are Google Map APIs (Map), Sendgrid (Email), and Twilio (SMS).

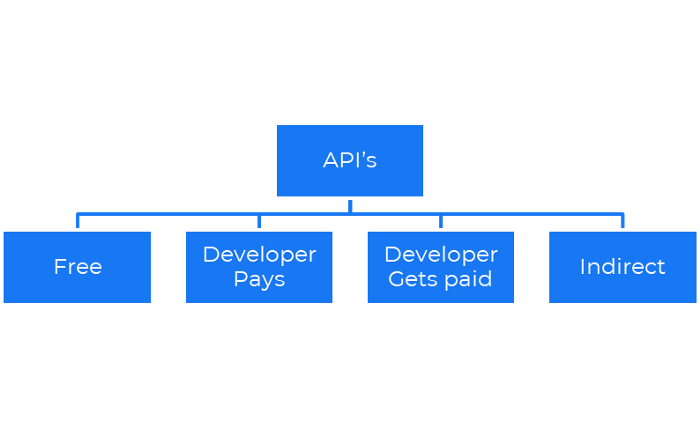

Business models for APIs

Free: The simplest API-driven business model that enables unrestricted API access for app developers. Google Translate and Facebook are two examples.

Developer Pays: Under this arrangement, service providers such as AWS, Twilio, Github, Stripe, and others must be paid by application developers.

The developer receives payment: These are the compensated content producers or developers who distribute the APIs utilizing their work. For example, Amazon affiliate programs

10. Open-source enterprise

Open-source software can be inspected, modified, and improved by anybody.

For instance, use Firefox, Java, or Android.

Google paid Mozilla $435,702 million to be their primary search engine in 2018.

Open-source software profits in six ways.

Paid assistance The Project Manager can charge for customization because he is quite knowledgeable about the codebase.

A full database solution is available as a Software as a Service (MongoDB Atlas), but there is a fee for the monitoring tool.

Open-core design R studio is a better GUI substitute for open-source applications.

sponsors of GitHub Sponsorships benefit the developers in full.

demands for paid features Earn Money By Developing Open Source Add-Ons for Current Products

Open-source business model

11. The business model for data

If the software or algorithm collects client data to improve or monetize the system.

Open AI GPT3 gets smarter with use.

Foursquare allows users to exchange check-in locations.

Later, they compiled large datasets to enable retailers like Starbucks launch new outlets.

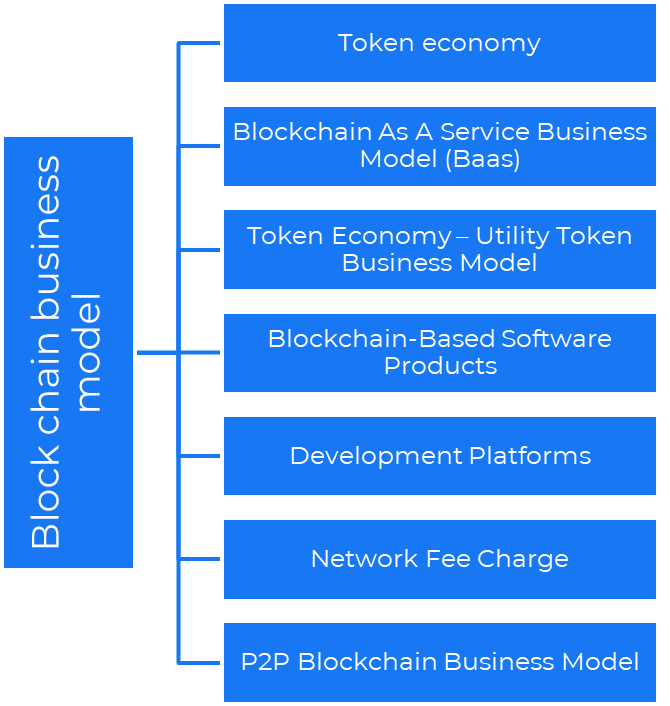

12. Business Model Using Blockchain

Blockchain is a distributed ledger technology that allows firms to deploy smart contracts without a central authority.

Examples include Alchemy, Solana, and Ethereum.

Business models using blockchain

Economy of tokens or utility When a business uses a token business model, it issues some kind of token as one of the ways to compensate token holders or miners. For instance, Solana and Ethereum

Bitcoin Cash P2P Business Model Peer-to-peer (P2P) blockchain technology permits direct communication between end users. as in IPFS

Enterprise Blockchain as a Service (Baas) BaaS focuses on offering ecosystem services similar to those offered by Amazon (AWS) and Microsoft (Azure) in the web 3 sector. Example: Ethereum Blockchain as a Service with Bitcoin (EBaaS).

Blockchain-Based Aggregators With AWS for blockchain, you can use that service by making an API call to your preferred blockchain. As an illustration, Alchemy offers nodes for many blockchains.

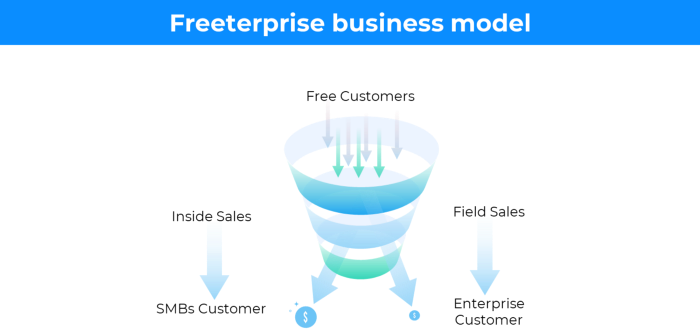

13. The free-enterprise model

In the freeterprise business model, free professional accounts are led into the funnel by the free product and later become B2B/enterprise accounts.

For instance, Slack and Zoom

Freeterprise companies flourish through collaboration.

Start with a free professional account to build an enterprise.

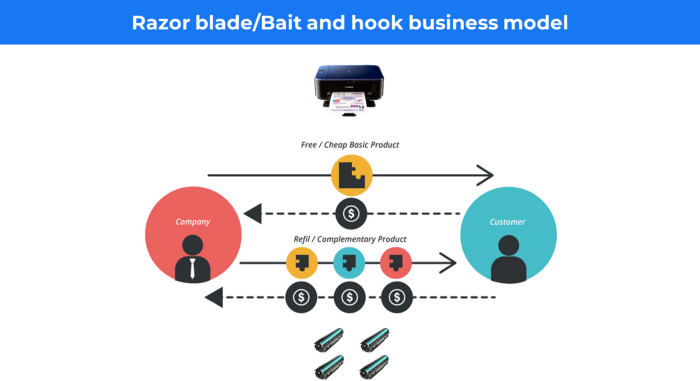

14. Business plan for razor blades

It's employed in hardware where one piece is sold at a loss and profits are made through refills or add-ons.

Gillet razor & blades, coffee machine & beans, HP printer & cartridge, etc.

Sony sells the Playstation console at a loss but makes up for it by selling games and charging for online services.

Advantages of the Razor-Razorblade Method

lowers the risk a customer will try a product. enables buyers to test the goods and services without having to pay a high initial investment.

The product's ongoing revenue stream has the potential to generate sales that much outweigh the original investments.

Razor blade business model

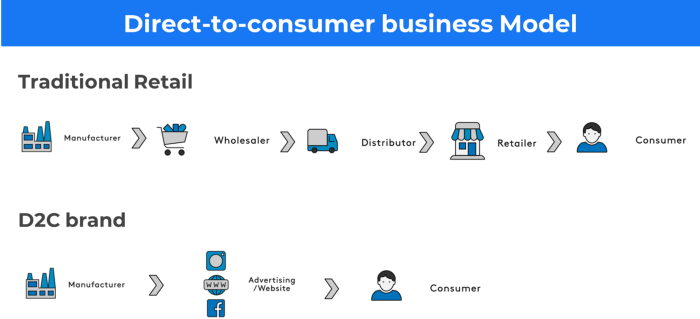

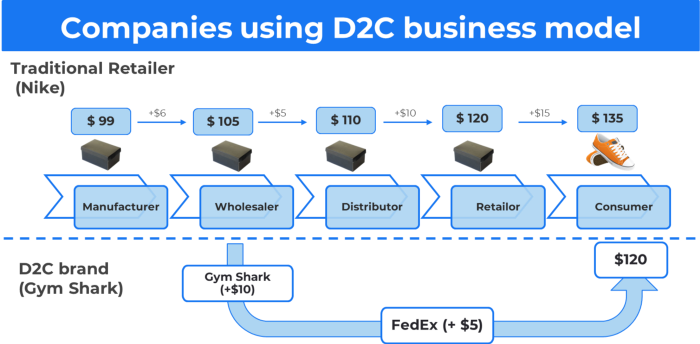

15. The business model of direct-to-consumer (D2C)

In D2C, the company sells directly to the end consumer through its website using a third-party logistic partner.

Examples include GymShark and Kylie Cosmetics.

D2C brands can only expand via websites, marketplaces (Amazon, eBay), etc.

D2C benefits

Lower reliance on middlemen = greater profitability

You now have access to more precise demographic and geographic customer data.

Additional space for product testing

Increased customisation throughout your entire product line-Inventory Less

16. Business model: White Label vs. Private Label

Private label/White label products are made by a contract or third-party manufacturer.

Most amazon electronics are made in china and white-labeled.

Amazon supplements and electronics.

Contract manufacturers handle everything after brands select product quantities on design labels.

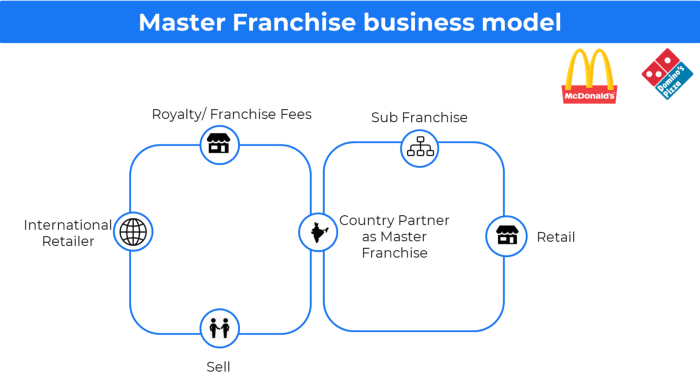

17. The franchise model

The franchisee uses the franchisor's trademark, branding, and business strategy (company).

For instance, KFC, Domino's, etc.

Subway, Domino, Burger King, etc. use this business strategy.

Many people pick a franchise because opening a restaurant is risky.

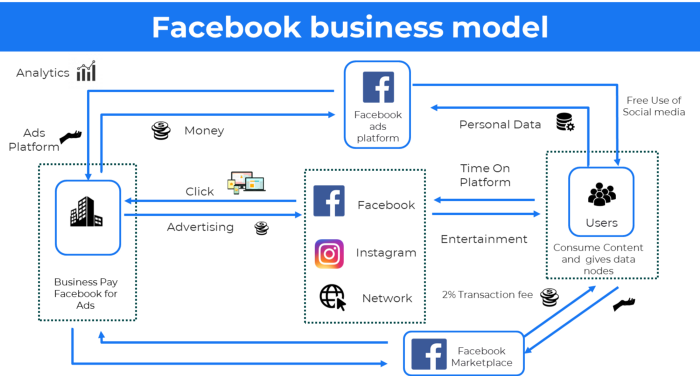

18. Ad-based business model

Social media and search engine giants exploit search and interest data to deliver adverts.

Google, Meta, TikTok, and Snapchat are some examples.

Users don't pay for the service or product given, e.g. Google users don't pay for searches.

In exchange, they collected data and hyper-personalized adverts to maximize revenue.

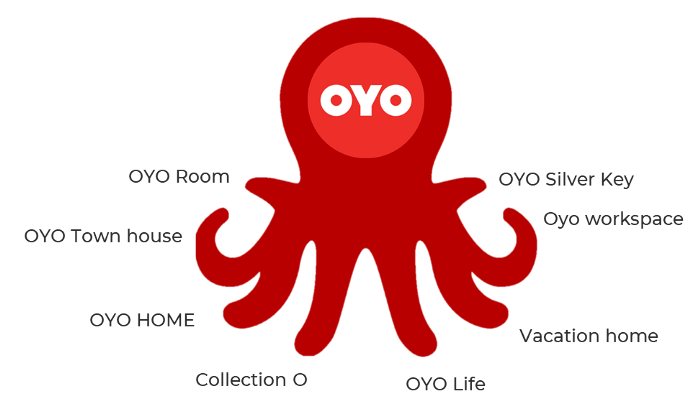

19. Business plan for octopuses

Each business unit functions separately but is connected to the main body.

Instance: Oyo

OYO is Asia's Airbnb, operating hotels, co-working, co-living, and vacation houses.

20, Transactional business model, number

Sales to customers produce revenue.

E-commerce sites and online purchases employ SSL.

Goli is an ex-GymShark.

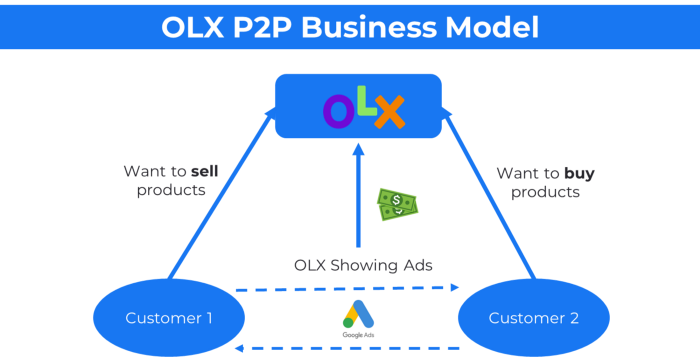

21. The peer-to-peer (P2P) business model

In P2P, two people buy and sell goods and services without a third party or platform.

Consider OLX.

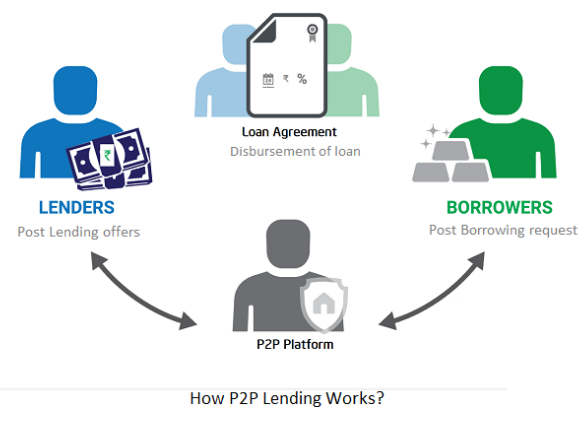

22. P2P lending as a manner of operation

In P2P lending, one private individual (P2P Lender) lends/invests or borrows money from another (P2P Borrower).

Instance: Kabbage

Social lending lets people lend and borrow money directly from each other without an intermediary financial institution.

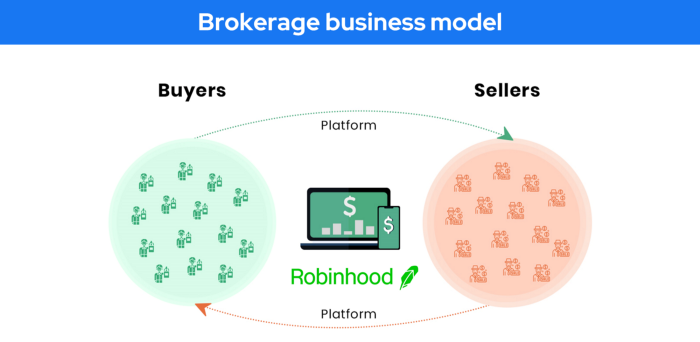

23. A business model for brokers

Brokerages charge a commission or fee for their services.

Examples include eBay, Coinbase, and Robinhood.

Brokerage businesses are common in Real estate, finance, and online and operate on this model.

Buy/sell similar models Examples include financial brokers, insurance brokers, and others who match purchase and sell transactions and charge a commission.

These brokers charge an advertiser a fee based on the date, place, size, or type of an advertisement. This is known as the classified-advertiser model. For instance, Craiglist

24. Drop shipping as an industry

Dropshipping allows stores to sell things without holding physical inventories.

When a customer orders, use a third-party supplier and logistic partners.

Retailer product portfolio and customer experience Fulfiller The consumer places the order.

Dropshipping advantages

Less money is needed (Low overhead-No Inventory or warehousing)

Simple to start (costs under $100)

flexible work environment

New product testing is simpler

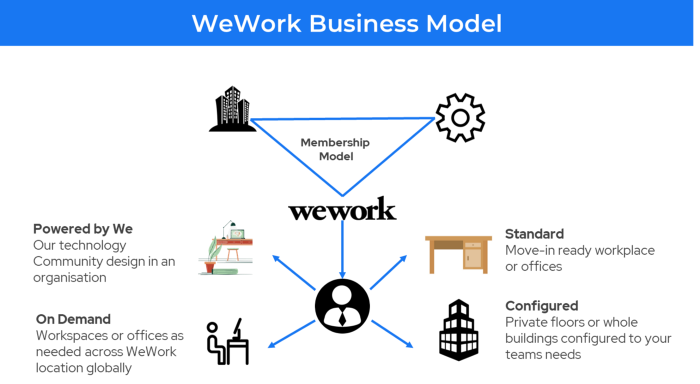

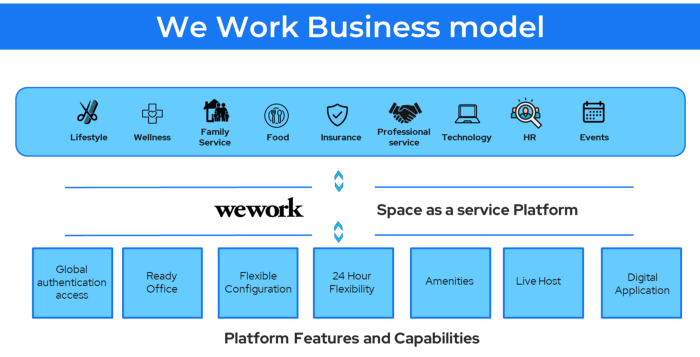

25. Business Model for Space as a Service

It's centered on a shared economy that lets millennials live or work in communal areas without ownership or lease.

Consider WeWork and Airbnb.

WeWork helps businesses with real estate, legal compliance, maintenance, and repair.

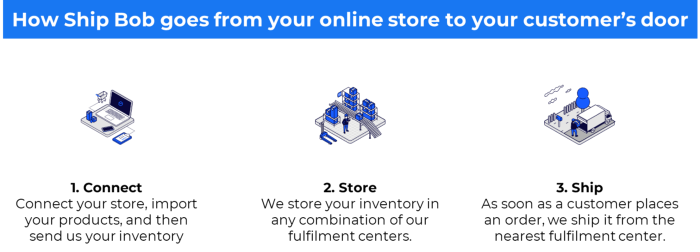

26. The business model for third-party logistics (3PL)

In 3PL, a business outsources product delivery, warehousing, and fulfillment to an external logistics company.

Examples include Ship Bob, Amazon Fulfillment, and more.

3PL partners warehouse, fulfill, and return inbound and outbound items for a charge.

Inbound logistics involves bringing products from suppliers to your warehouse.

Outbound logistics refers to a company's production line, warehouse, and customer.

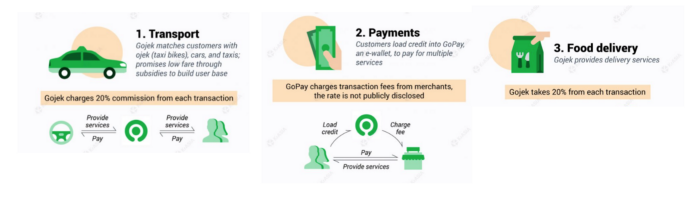

27. The last-mile delivery paradigm as a commercial strategy

Last-mile delivery is the collection of supply chain actions that reach the end client.

Examples include Rappi, Gojek, and Postmates.

Last-mile is tied to on-demand and has a nighttime peak.

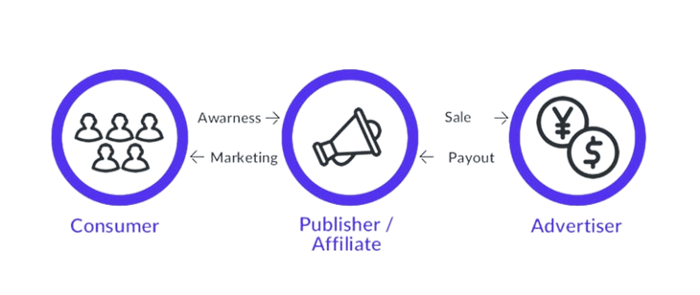

28. The use of affiliate marketing

Affiliate marketing involves promoting other companies' products and charging commissions.

Examples include Hubspot, Amazon, and Skillshare.

Your favorite youtube channel probably uses these short amazon links to get 5% of sales.

Affiliate marketing's benefits

In exchange for a success fee or commission, it enables numerous independent marketers to promote on its behalf.

Ensure system transparency by giving the influencers a specific tracking link and an online dashboard to view their profits.

Learn about the newest bargains and have access to promotional materials.

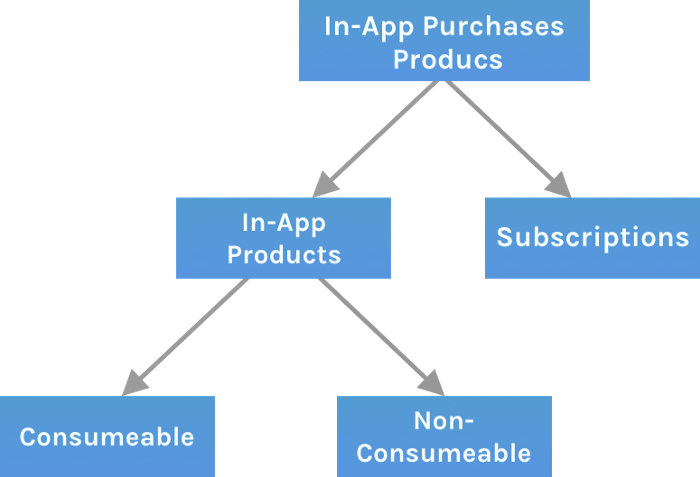

29. The business model for virtual goods

This is an in-app purchase for an intangible product.

Examples include PubG, Roblox, Candy Crush, etc.

Consumables are like gaming cash that runs out. Non-consumable products provide a permanent advantage without repeated purchases.

30. Business Models for Cloud Kitchens

Ghost, Dark, Black Box, etc.

Delivery-only restaurant.

These restaurants don't provide dine-in, only delivery.

For instance, NextBite and Faasos

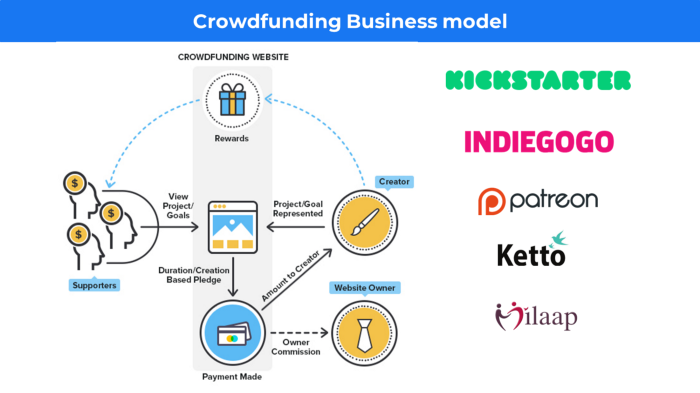

31. Crowdsourcing as a Business Model

Crowdsourcing = Using the crowd as a platform's source.

In crowdsourcing, you get support from people around the world without hiring them.

Crowdsourcing sites

Open-Source Software gives access to the software's source code so that developers can edit or enhance it. Examples include Firefox browsers and Linux operating systems.

Crowdfunding The oculus headgear would be an example of crowdfunding in essence, with no expectations.

Khoi Ho

3 years ago

After working at seven startups, here are the early-stage characteristics that contributed to profitability, unicorn status or successful acquisition.

I've worked in a People role at seven early-stage firms for over 15 years (I enjoy chasing a dream!). Few of the seven achieved profitability, including unicorn status or acquisition.

Did early-stage startups share anything? Was there a difference between winners and losers? YES.

I support founders and entrepreneurs building financially sustainable enterprises with a compelling cause. This isn't something everyone would do. A company's success demands more than guts. Founders drive startup success.

Six Qualities of Successful Startups

Successful startup founders either innately grasped the correlation between strong team engagement and a well-executed business model, or they knew how to ask and listen to others (executive coaches, other company leaders, the team itself) to learn about it.

Successful startups:

1. Co-founders agreed and got along personally.

Multi-founder startups are common. When co-founders agree on strategic decisions and are buddies, there's less friction and politics at work.

As a co-founder, ask your team if you're aligned. They'll explain.

I've seen C-level leaders harbor personal resentments over disagreements. A co-departure founder's caused volatile leadership and work disruptions that the team struggled to manage during and after.

2. Team stayed.

Successful startups have low turnover. Nobody is leaving. There may be a termination for performance, but other team members will have observed the issues and agreed with the decision.

You don't want organizational turnover of 30%+, with leaders citing performance issues but the team not believing them. This breeds suspicion.

Something is wrong if many employees leave voluntarily or involuntarily. You may hear about lack of empowerment, support, or toxic leadership in exit interviews and from the existing team. Intellectual capital loss and resource instability harm success.

3. Team momentum.

A successful startup's team is excited about its progress. Consistently achieving goals and having trackable performance metrics. Some describe this period of productivity as magical, with great talents joining the team and the right people in the right places. Increasing momentum.

I've also seen short-sighted decisions where only some departments, like sales and engineering, had goals. Lack of a unified goals system created silos and miscommunication. Some employees felt apathetic because they didn't know how they contributed to team goals.

4. Employees advanced in their careers.

Even if you haven't created career pathing or professional development programs, early-stage employees will grow and move into next-level roles. If you hire more experienced talent and leaders, expect them to mentor existing team members. Growing companies need good performers.

New talent shouldn't replace and discard existing talent. This creates animosity and makes existing employees feel unappreciated for their early contributions to the company.

5. The company lived its values.

Culture and identity are built on lived values. A company's values affect hiring, performance management, rewards, and other processes. Identify, practice, and believe in company values. Starting with team values instead of management or consultants helps achieve this. When a company's words and actions match, it builds trust.

When company values are beautifully displayed on a wall but few employees understand them, the opposite is true. If an employee can't name the company values, they're useless.

6. Communication was clear.

When necessary information is shared with the team, they feel included, trusted, and like owners. Transparency means employees have the needed information to do their jobs. Disclosure builds trust. The founders answer employees' questions honestly.

Information accessibility decreases office politics. Without transparency, even basic information is guarded and many decisions are made in secret. I've seen founders who don't share financial, board meeting, or compensation and equity information. The founders' lack of trust in the team wasn't surprising, so it was reciprocated.

The Choices

Finally. All six of the above traits (leadership alignment, minimal turnover, momentum, professional advancement, values, and transparency) were high in the profitable startups I've worked at, including unicorn status or acquisition.

I've seen these as the most common and constant signals of startup success or failure.

These characteristics are the product of founders' choices. These decisions lead to increased team engagement and business execution.

Here's something to consider for startup employees and want-to-bes. 90% of startups fail, despite the allure of building something new and gaining ownership. With the emotional and time investment in startup formation, look for startups with these traits to reduce your risk.

Both you and the startup will thrive in these workplaces.

Edward Williams

3 years ago

I currently manage 4 profitable online companies. I find all the generic advice and garbage courses very frustrating. The only advice you need is this.

This is for young entrepreneurs, especially in tech.

People give useless success advice on TikTok and Reddit. Early risers, bookworms, etc. Entrepreneurship courses. Work hard and hustle.

False. These aren't successful traits.

I mean, organization is good. As someone who founded several businesses and now works at a VC firm, I find these tips to be clichés.

Based on founding four successful businesses and working with other successful firms, here's my best actionable advice:

1. Choose a sector or a niche and become an expert in it.

This is more generic than my next tip, but it's a must-do that's often overlooked. Become an expert in the industry or niche you want to enter. Discover everything.

Buy (future) competitors' products. Understand consumers' pain points. Market-test. Target keyword combos. Learn technical details.

The most successful businesses I've worked with were all formed by 9-5 employees. They knew the industry's pain points. They started a business targeting these pain points.

2. Choose a niche or industry crossroads to target.

How do you choose an industry or niche? What if your industry is too competitive?

List your skills and hobbies. Randomness is fine. Find an intersection between two interests or skills.

Say you build websites well. You like cars.

Web design is a *very* competitive industry. Cars and web design?

Instead of web design, target car dealers and mechanics. Build a few fake demo auto mechanic websites, then cold call shops with poor websites. Verticalize.

I've noticed a pattern:

Person works in a particular industry for a corporation.

Person gains expertise in the relevant industry.

Person quits their job and launches a small business to address a problem that their former employer was unwilling to address.

I originally posted this on Reddit and it seemed to have taken off so I decided to share it with you all.

Focus on the product. When someone buys from you, you convince them the product's value exceeds the price. It's not fair and favors the buyer.

Creating a superior product or service will win. Narrowing this helps you outcompete others.

You may be their only (lucky) option.

You might also like

Yogita Khatri

4 years ago

Moonbirds NFT sells for $1 million in first week

On Saturday, Moonbird #2642, one of the collection's rarest NFTs, sold for a record 350 ETH (over $1 million) on OpenSea.

The Sandbox, a blockchain-based gaming company based in Hong Kong, bought the piece. The seller, "oscuranft" on OpenSea, made around $600,000 after buying the NFT for 100 ETH a week ago.

Owl avatars

Moonbirds is a 10,000 owl NFT collection. It is one of the quickest collections to achieve bluechip status. Proof, a media startup founded by renowned VC Kevin Rose, launched Moonbirds on April 16.

Rose is currently a partner at True Ventures, a technology-focused VC firm. He was a Google Ventures general partner and has 1.5 million Twitter followers.

Rose has an NFT podcast on Proof. It follows Proof Collective, a group of 1,000 NFT collectors and artists, including Beeple, who hold a Proof Collective NFT and receive special benefits.

These include early access to the Proof podcast and in-person events.

According to the Moonbirds website, they are "the official Proof PFP" (picture for proof).

Moonbirds NFTs sold nearly $360 million in just over a week, according to The Block Research and Dune Analytics. Its top ten sales range from $397,000 to $1 million.

In the current market, Moonbirds are worth 33.3 ETH. Each NFT is 2.5 ETH. Holders have gained over 12 times in just over a week.

Why was it so popular?

The Block Research's NFT analyst, Thomas Bialek, attributes Moonbirds' rapid rise to Rose's backing, the success of his previous Proof Collective project, and collectors' preference for proven NFT projects.

Proof Collective NFT holders have made huge gains. These NFTs were sold in a Dutch auction last December for 5 ETH each. According to OpenSea, the current floor price is 109 ETH.

According to The Block Research, citing Dune Analytics, Proof Collective NFTs have sold over $39 million to date.

Rose has bigger plans for Moonbirds. Moonbirds is introducing "nesting," a non-custodial way for holders to stake NFTs and earn rewards.

Holders of NFTs can earn different levels of status based on how long they keep their NFTs locked up.

"As you achieve different nest status levels, we can offer you different benefits," he said. "We'll have in-person meetups and events, as well as some crazy airdrops planned."

Rose went on to say that Proof is just the start of "a multi-decade journey to build a new media company."

Christianlauer

3 years ago

Looker Studio Pro is now generally available, according to Google.

Great News about the new Google Business Intelligence Solution

Google has renamed Data Studio to Looker Studio and Looker Studio Pro.

Now, Google releases Looker Studio Pro. Similar to the move from Data Studio to Looker Studio, Looker Studio Pro is basically what Looker was previously, but both solutions will merge. Google says the Pro edition will acquire new enterprise management features, team collaboration capabilities, and SLAs.

![Dashboard Example in Looker Studio Pro — Image Source: Google[2]](https://storage.googleapis.com/int3grity/posts/m9yb4IqJCm7D/images/ZuJudlWT6GUeTKKNVduA5)

In addition to Google's announcements and sales methods, additional features include:

Looker Studio assets can now have organizational ownership. Customers can link Looker Studio to a Google Cloud project and migrate existing assets once. This provides:

Your users' created Looker Studio assets are all kept in a Google Cloud project.

When the users who own assets leave your organization, the assets won't be removed.

Using IAM, you may provide each Looker Studio asset in your company project-level permissions.

Other Cloud services can access Looker Studio assets that are owned by a Google Cloud project.

Looker Studio Pro clients may now manage report and data source access at scale using team workspaces.

Google announcing these features for the pro version is fascinating. Both products will likely converge, but Google may only release many features in the premium version in the future. Microsoft with Power BI and its free and premium variants already achieves this.

Sources and Further Readings

Google, Release Notes (2022)

Google, Looker (2022)

William Brucee

3 years ago

This person is probably Satoshi Nakamoto.

Who founded bitcoin is the biggest mystery in technology today, not how it works.

On October 31, 2008, Satoshi Nakamoto posted a whitepaper to a cryptography email list. Still confused by the mastermind who changed monetary history.

Journalists and bloggers have tried in vain to uncover bitcoin's creator. Some candidates self-nominated. We're still looking for the mystery's perpetrator because none of them have provided proof.

One person. I'm confident he invented bitcoin. Let's assess Satoshi Nakamoto before I reveal my pick. Or what he wants us to know.

Satoshi's P2P Foundation biography says he was born in 1975. He doesn't sound or look Japanese. First, he wrote the whitepaper and subsequent articles in flawless English. His sleeping habits are unusual for a Japanese person.

Stefan Thomas, a Bitcoin Forum member, displayed Satoshi's posting timestamps. Satoshi Nakamoto didn't publish between 2 and 8 p.m., Japanese time. Satoshi's identity may not be real.

Why would he disguise himself?

There is a legitimate explanation for this

Phil Zimmermann created PGP to give dissidents an open channel of communication, like Pretty Good Privacy. US government seized this technology after realizing its potential. Police investigate PGP and Zimmermann.

This technology let only two people speak privately. Bitcoin technology makes it possible to send money for free without a bank or other intermediary, removing it from government control.

How much do we know about the person who invented bitcoin?

Here's what we know about Satoshi Nakamoto now that I've covered my doubts about his personality.

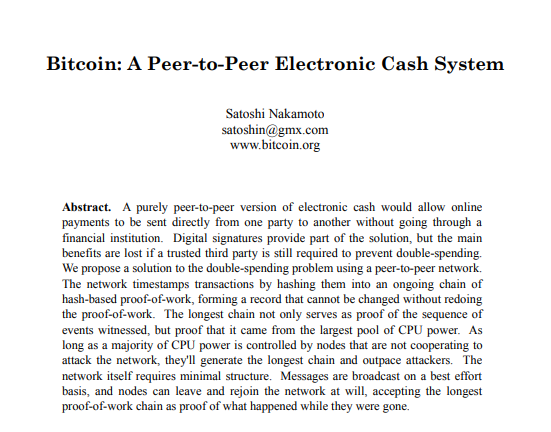

Satoshi Nakamoto first appeared with a whitepaper on metzdowd.com. On Halloween 2008, he presented a nine-page paper on a new peer-to-peer electronic monetary system.

Using the nickname satoshi, he created the bitcointalk forum. He kept developing bitcoin and created bitcoin.org. Satoshi mined the genesis block on January 3, 2009.

Satoshi Nakamoto worked with programmers in 2010 to change bitcoin's protocol. He engaged with the bitcoin community. Then he gave Gavin Andresen the keys and codes and transferred community domains. By 2010, he'd abandoned the project.

The bitcoin creator posted his goodbye on April 23, 2011. Mike Hearn asked Satoshi if he planned to rejoin the group.

“I’ve moved on to other things. It’s in good hands with Gavin and everyone.”

Nakamoto Satoshi

The man who broke the banking system vanished. Why?

Satoshi's wallets held 1,000,000 BTC. In December 2017, when the price peaked, he had over US$19 billion. Nakamoto had the 44th-highest net worth then. He's never cashed a bitcoin.

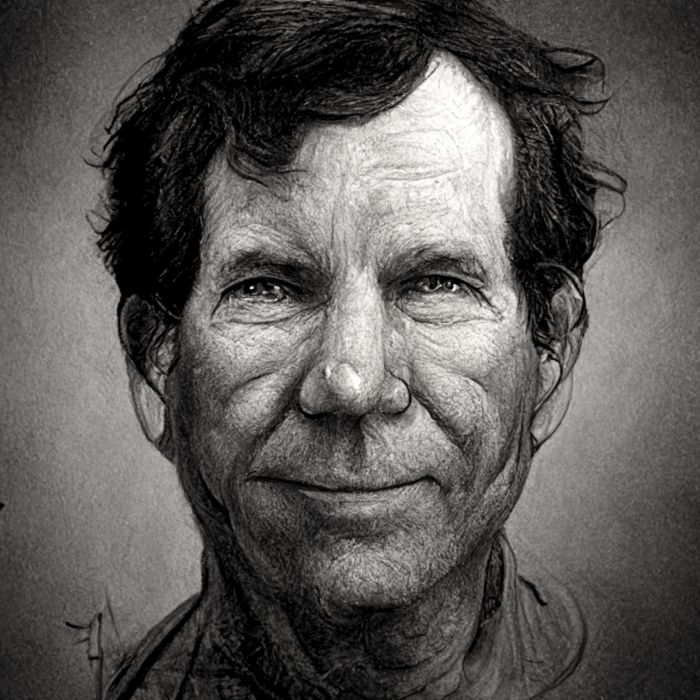

This data suggests something happened to bitcoin's creator. I think Hal Finney is Satoshi Nakamoto .

Hal Finney had ALS and died in 2014. I suppose he created the future of money, then he died, leaving us with only rumors about his identity.

Hal Finney, who was he?

Hal Finney graduated from Caltech in 1979. Student peers voted him the smartest. He took a doctoral-level gravitational field theory course as a freshman. Finney's intelligence meets the first requirement for becoming Satoshi Nakamoto.

Students remember Finney holding an Ayn Rand book. If he'd read this, he may have developed libertarian views.

His beliefs led him to a small group of freethinking programmers. In the 1990s, he joined Cypherpunks. This action promoted the use of strong cryptography and privacy-enhancing technologies for social and political change. Finney helped them achieve a crypto-anarchist perspective as self-proclaimed privacy defenders.

Zimmermann knew Finney well.

Hal replied to a Cypherpunk message about Phil Zimmermann and PGP. He contacted Phil and became PGP Corporation's first member, retiring in 2011. Satoshi Nakamoto quit bitcoin in 2011.

Finney improved the new PGP protocol, but he had to do so secretly. He knew about Phil's PGP issues. I understand why he wanted to hide his identity while creating bitcoin.

Why did he pretend to be from Japan?

His envisioned persona was spot-on. He resided near scientist Dorian Prentice Satoshi Nakamoto. Finney could've assumed Nakamoto's identity to hide his. Temple City has 36,000 people, so what are the chances they both lived there? A cryptographic genius with the same name as Bitcoin's creator: coincidence?

Things went differently, I think.

I think Hal Finney sent himself Satoshis messages. I know it's odd. If you want to conceal your involvement, do as follows. He faked messages and transferred the first bitcoins to himself to test the transaction mechanism, so he never returned their money.

Hal Finney created the first reusable proof-of-work system. The bitcoin protocol. In the 1990s, Finney was intrigued by digital money. He invented CRypto cASH in 1993.

Legacy

Hal Finney's contributions should not be forgotten. Even if I'm wrong and he's not Satoshi Nakamoto, we shouldn't forget his bitcoin contribution. He helped us achieve a better future.