More on Society & Culture

Katharine Valentino

3 years ago

A Gun-toting Teacher Is Like a Cook With Rat Poison

Pink or blue AR-15s?

A teacher teaches; a gun kills. Killing isn't teaching. Killing is opposite of teaching.

Without 27 school shootings this year, we wouldn't be talking about arming teachers. Gun makers, distributors, and the NRA cause most school shootings. Gun makers, distributors, and the NRA wouldn't be huge business if weapons weren't profitable.

Guns, ammo, body armor, holsters, concealed carriers, bore sights, cleaner kits, spare magazines and speed loaders, gun safes, and ear protection are sold. And more guns.

And lots more profit.

Guns aren't bread. You eat a loaf of bread in a week or so and then must buy more. Bread makers will make money. Winchester 94.30–30 1899 Lever Action Rifle from 1894 still kills. (For safety, I won't link to the ad.) Gun makers don't object if you collect antique weapons, but they need you to buy the latest, in-style killing machine. The youngster who killed 19 students and 2 teachers at Robb Elementary School in Uvalde, Texas, used an AR-15. Better yet, two.

Salvador Ramos, the Robb Elementary shooter, is a "killing influencer" He pushes consumers to buy items, which benefits manufacturers and distributors. Like every previous AR-15 influencer, he profits Colt, the rifle's manufacturer, and 52,779 gun dealers in the U.S. Ramos and other AR-15 influences make us fear for our safety and our children's. Fearing for our safety, we acquire 20 million firearms a year and live in a gun culture.

So now at school, we want to arm teachers.

Consider. Which of your teachers would you have preferred in body armor with a gun drawn?

Miss Summers? Remember her bringing daisies from her yard to second grade? She handed each student a beautiful flower. Miss Summers loved everyone, even those with AR-15s. She can't shoot.

Frasier? Mr. Frasier turned a youngster over down to explain "invert." Mr. Frasier's hands shook when he wasn't flipping fifth-graders and fractions. He may have shot wrong.

Mrs. Barkley barked in high school English class when anyone started an essay with "But." Mrs. Barkley dubbed Abie a "Jewboy" and gave him terrible grades. Arming Miss Barkley is like poisoning the chef.

Think back. Do you remember a teacher with a gun? No. Arming teachers so the gun industry can make more money is the craziest idea ever.

Or maybe you agree with Ted Cruz, the gun lobby-bought senator, that more guns reduce gun violence. After the next school shooting, you'll undoubtedly talk about arming teachers and pupils. Colt will likely develop a backpack-sized, lighter version of its popular killing machine in pink and blue for kids and boys. The MAR-15? (M for mini).

This post is a summary. Read the full one here.

Jack Shepherd

3 years ago

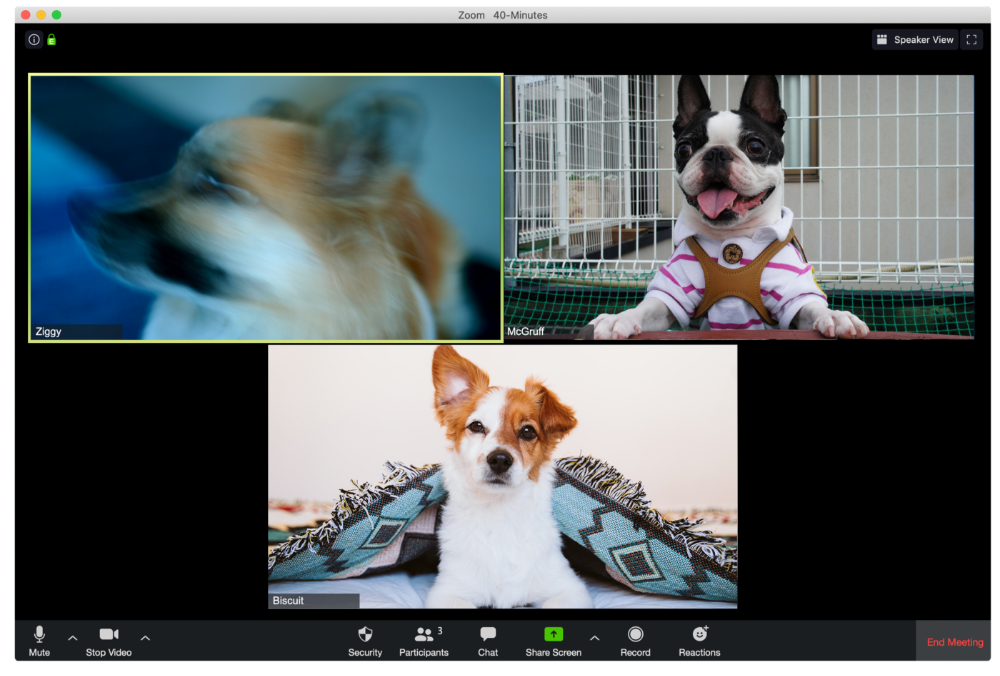

A Dog's Guide to Every Type of Zoom Call Participant

Are you one of these Zoom dogs?

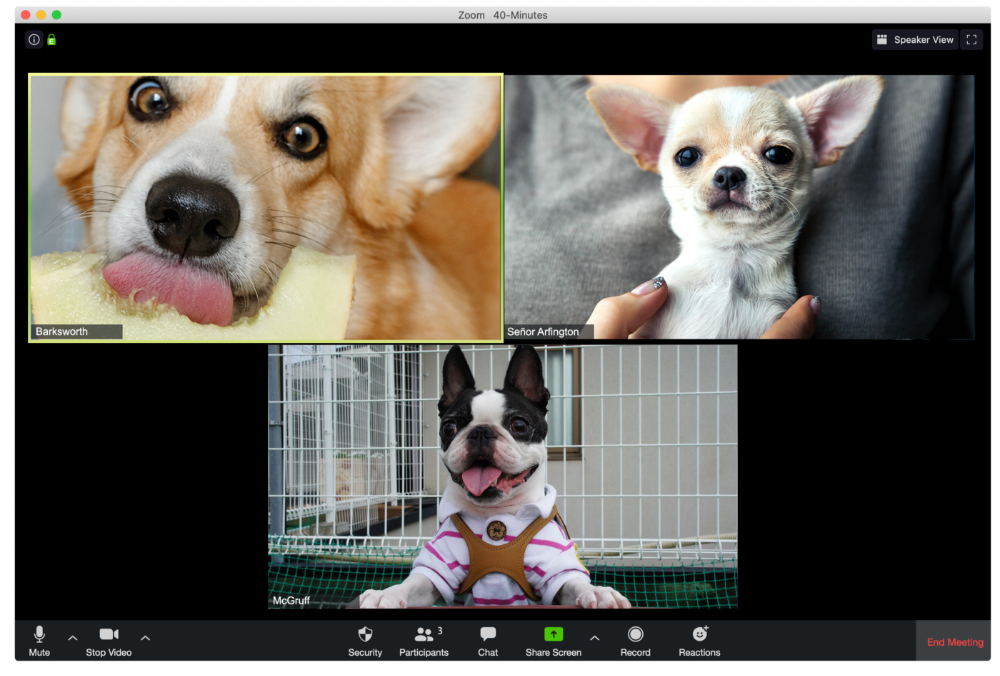

The Person Who Is Apparently Always on Mute

Waffles thinks he can overpower the mute button by shouting loudly.

The person who believed their camera to be off

Barkley's used to remote work, but he hasn't mastered the "Stop Video" button. Everyone is affected.

Who is driving for some reason, exactly?

Why is Pumpkin always late? Who knows? Shouldn't she be driving? If you could hear her over the freeway, she'd answer these questions.

The Person With the Amazing Bookcase

Cicero likes to use SAT-words like "leverage" and "robust" in Zoom sessions, presumably from all the books he wants you to see behind him.

The Individual Who Is Unnecessarily Dressed

We hope Bandit is going somewhere beautiful after this meeting, or else he neglected the quarterly earnings report and is overcompensating to distract us.

The person who works through lunch in between zoom calls

Barksworth has back-to-back meetings all day, so you can watch her eat while she talks.

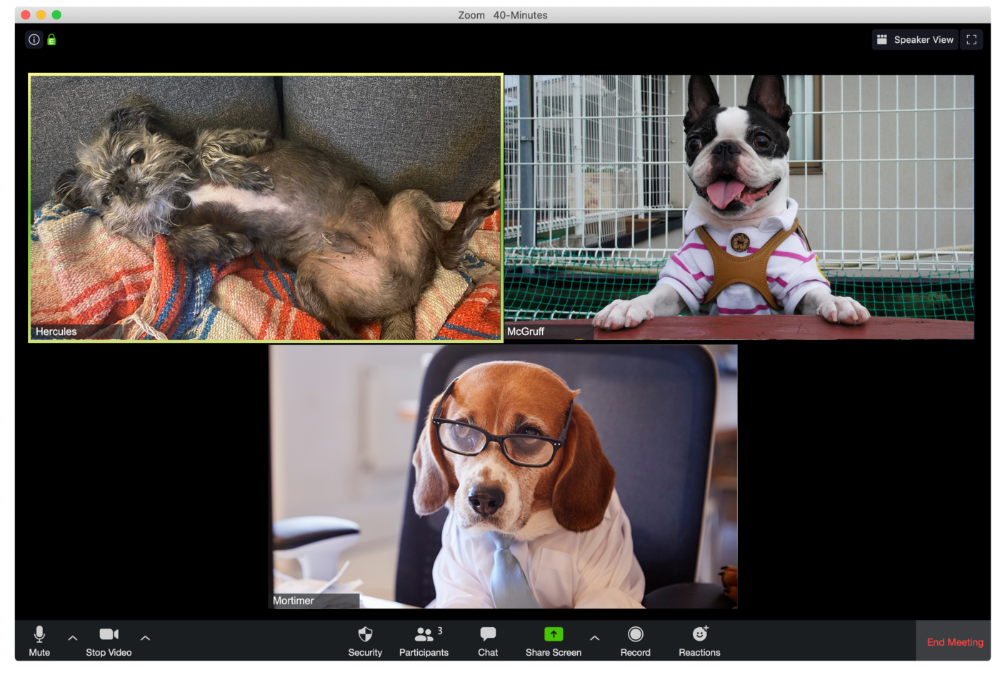

The Person Who Is A Little Too Comfy

Hercules thinks Zoom meetings happen between sleeps. He'd appreciate everyone speaking more quietly.

The Person Who Answered the Phone Outside

Frisbee has a gorgeous backyard and lives in a place with great weather year-round, and she wants you to think about that during the daily team huddle.

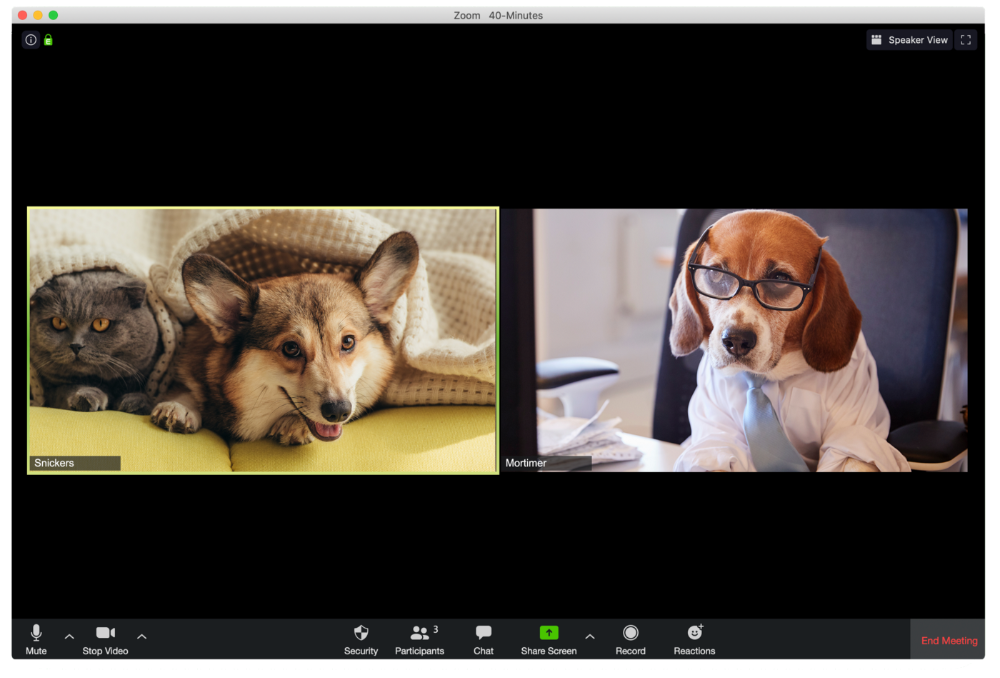

Who Wants You to Pay Attention to Their Pet

Snickers hasn't listened to you in 20 minutes unless you tell her how cute her kitten is.

One who is, for some reason, positioned incorrectly on the screen

Nelson's meetings consist primarily of attempting to figure out how he positioned his laptop so absurdly.

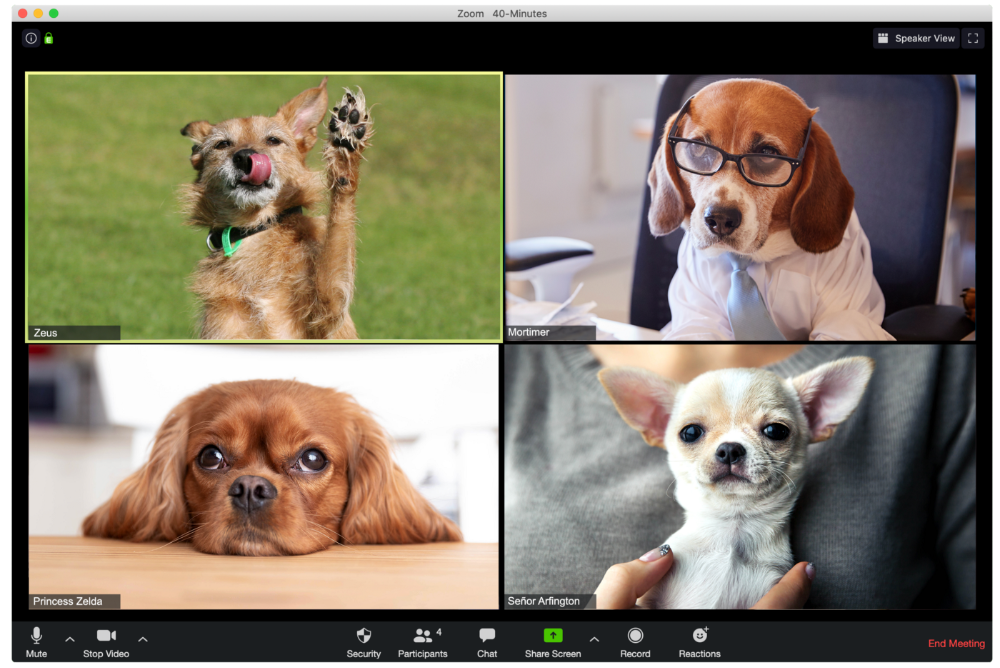

The person who says too many goodbyes

Zeus waves farewell like it's your first day of school while everyone else searches for the "Leave Meeting" button. It's nice.

He who has a poor internet connection

Ziggy's connectivity problems continue... She gives a long speech as everyone waits awkwardly to inform her they missed it.

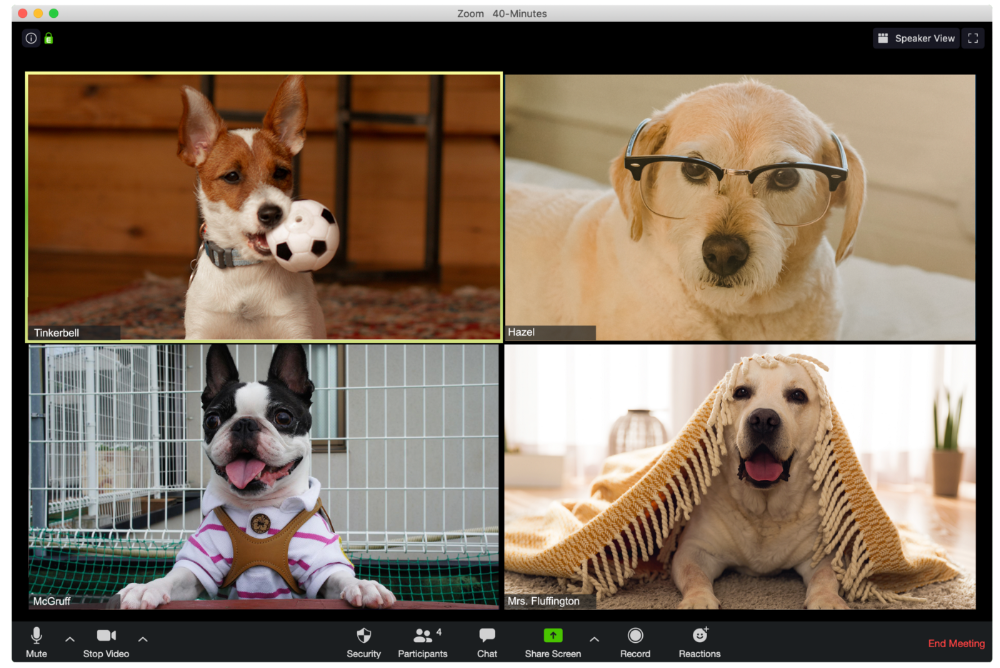

The Clearly Multitasking Person

Tinkerbell can play fetch during the monthly staff meeting if she works from home, but that's not a good idea.

The Person Using Zoom as a Makeup and Hair Mirror

If Gail and Bob knew Zoom had a "hide self view" option, they'd be distraught.

The person who feels at ease with simply leaving

Rusty bails when a Zoom conference is over. Rusty's concept is decent.

Hudson Rennie

3 years ago

Meet the $5 million monthly controversy-selling King of Toxic Masculinity.

Trigger warning — Andrew Tate is running a genius marketing campaign

Andrew Tate is a 2022 internet celebrity.

Kickboxing world champion became rich playboy with controversial views on gender roles.

Andrew's get-rich-quick scheme isn't new. His social media popularity is impressive.

He’s currently running one of the most genius marketing campaigns in history.

He pulls society's pendulum away from diversity and inclusion and toward diversion and exclusion. He's unstoppable.

Here’s everything you need to know about Andrew Tate. And how he’s playing chess while the world plays checkers.

Cobra Tate is the name he goes by.

American-born, English-raised entrepreneur Andrew Tate lives in Romania.

Romania? Says Andrew,

“I prefer a country in which corruption is available to everyone.”

Andrew was a professional kickboxer with the ring moniker Cobra before starting Hustlers University.

Before that, he liked chess and worshipped his father.

Emory Andrew Tate III is named after his grandmaster chess player father.

Emory was the first black-American chess champion. He was military, martial arts-trained, and multilingual. A superhuman.

He lived in his car to make ends meet.

Andrew and Tristan relocated to England with their mother when their parents split.

It was there that Andrew began his climb toward becoming one of the internet’s greatest villains.

Andrew fell in love with kickboxing.

Andrew spent his 20s as a professional kickboxer and reality TV star, featuring on Big Brother UK and The Ultimate Traveller.

These 3 incidents, along with a chip on his shoulder, foreshadowed Andrews' social media breakthrough.

Chess

Combat sports

Reality television

A dangerous trio.

Andrew started making money online after quitting kickboxing in 2017 due to an eye issue.

Andrew didn't suddenly become popular.

Andrew's web work started going viral in 2022.

Due to his contentious views on patriarchy and gender norms, he's labeled the King of Toxic Masculinity. His most contentious views (trigger warning):

“Women are intrinsically lazy.”

“Female promiscuity is disgusting.”

“Women shouldn’t drive cars or fly planes.”

“A lot of the world’s problems would be solved if women had their body count tattooed on their foreheads.”

Andrew's two main beliefs are:

“These are my personal opinions based on my experiences.”

2. “I believe men are better at some things and women are better at some things. We are not equal.”

Andrew intentionally offends.

Andrew's thoughts began circulating online in 2022.

In July 2022, he was one of the most Googled humans, surpassing:

Joe Biden

Donald Trump

Kim Kardashian

Andrews' rise is a mystery since no one can censure or suppress him. This is largely because Andrew nor his team post his clips.

But more on that later.

Andrew's path to wealth.

Andrew Tate is a self-made millionaire. His morality is uncertain.

Andrew and Tristan needed money soon after retiring from kickboxing.

“I owed some money to some dangerous people. I had $70K and needed $100K to stay alive.”

Andrews lost $20K on roulette at a local casino.

Andrew had one week to make $50,000, so he started planning. Andrew locked himself in a chamber like Thomas Edison to solve an energy dilemma.

He listed his assets.

Physical strength (but couldn’t fight)

a BMW (worth around $20K)

Intelligence (but no outlet)

A lightbulb.

He had an epiphany after viewing a webcam ad. He sought aid from women, ironically. His 5 international girlfriends are assets.

Then, a lightbulb.

Andrew and Tristan messaged and flew 7 women to a posh restaurant. Selling desperation masked as opportunity, Andrew pitched his master plan:

A webcam business — with a 50/50 revenue split.

5 women left.

2 stayed.

Andrew Tate, a broke kickboxer, became Top G, Cobra Tate.

The business model was simple — yet sad.

Andrew's girlfriends moved in with him and spoke online for 15+ hours a day. Andrew handled ads and equipment as the women posed.

Andrew eventually took over their keyboards, believing he knew what men wanted more than women.

Andrew detailed on the Full Send Podcast how he emotionally manipulated men for millions. They sold houses, automobiles, and life savings to fuel their companionship addiction.

When asked if he felt bad, Andrew said,

“F*ck no.“

Andrew and Tristan wiped off debts, hired workers, and diversified.

Tristan supervised OnlyFans models.

Andrew bought Romanian casinos and MMA league RXF (Real Xtreme Fighting).

Pandemic struck suddenly.

Andrew couldn't run his 2 businesses without a plan. Another easy moneymaker.

He banked on Hustlers University.

The actual cause of Andrew's ubiquity.

On a Your Mom’s House episode Andrew's 4 main revenue sources:

Hustler’s University

2. Owning casinos in Romania

3. Owning 10% of the Romanian MMA league “RXF”

4. “The War Room” — a society of rich and powerful men

When the pandemic hit, 3/4 became inoperable.

So he expanded Hustlers University.

But what is Hustler’s University?

Andrew says Hustlers University teaches 18 wealth-building tactics online. Examples:

Real estate

Copywriting

Amazon FBA

Dropshipping

Flipping Cryptos

How to swiftly become wealthy.

Lessons are imprecise, rudimentary, and macro-focused, say reviews. Invest wisely, etc. Everything is free online.

You pay for community. One unique income stream.

The only money-making mechanism that keeps the course from being a scam.

The truth is, many of Andrew’s students are actually making money. Maybe not from the free YouTube knowledge Andrew and his professors teach in the course, but through Hustler’s University’s affiliate program.

Affiliates earn 10% commission for each new student = $5.

Students can earn $10 for each new referral in the first two months.

Andrew earns $50 per membership per month.

This affiliate program isn’t anything special — in fact, it’s on the lower end of affiliate payouts. Normally, it wouldn’t be very lucrative.

But it has one secret weapon— Andrew and his viral opinions.

Andrew is viral. Andrew went on a media tour in January 2022 after appearing on Your Mom's House.

And many, many more…

He chatted with Twitch streamers. Hustlers University wanted more controversy (and clips).

Here’s the strategy behind Hustler’s University that has (allegedly) earned students upwards of $10K per month:

Make a social media profile with Andrew Tates' name and photo.

Post any of the online videos of Andrews that have gone viral.

Include a referral link in your bio.

Effectively simple.

Andrew's controversy attracts additional students. More student clips circulate as more join. Andrew's students earn more and promote the product as he goes viral.

A brilliant plan that's functioning.

At the beginning of his media tour, Hustler’s University had 5,000 students. 6 months in, and he now has over 100,000.

One income stream generates $5 million every month.

Andrew's approach is not new.

But it is different.

In the early 2010s, Tai Lopez dominated the internet.

His viral video showed his house.

“Here in my garage. Just bought this new Lamborghini.”

Tais' marketing focused on intellect, not strength, power, and wealth to attract women.

How reading quicker leads to financial freedom in 67 steps.

Years later, it was revealed that Tai Lopez rented the mansion and Lamborghini as a marketing ploy to build social proof. Meanwhile, he was living in his friend’s trailer.

Faked success is an old tactic.

Andrew is doing something similar. But with one major distinction.

Andrew outsources his virality — making him nearly impossible to cancel.

In 2022, authorities searched Andrews' estate over human trafficking suspicions. Investigation continues despite withdrawn charges.

Andrew's divisive nature would normally get him fired. Andrew's enterprises and celebrity don't rely on social media.

He doesn't promote or pay for ads. Instead, he encourages his students and anyone wishing to get rich quick to advertise his work.

Because everything goes through his affiliate program. Old saying:

“All publicity is good publicity.”

Final thoughts: it’s ok to feel triggered.

Tate is divisive.

His emotionally charged words are human nature. Andrews created the controversy.

It's non-personal.

His opinions are those of one person. Not world nor generational opinion.

Briefly:

It's easy to understand why Andrews' face is ubiquitous. Money.

The world wide web is a chessboard. Misdirection is part of it.

It’s not personal, it’s business.

Controversy sells

Sometimes understanding the ‘why’, can help you deal with the ‘what.’

You might also like

Tim Denning

3 years ago

I gave up climbing the corporate ladder once I realized how deeply unhappy everyone at the top was.

Restructuring and layoffs cause career reevaluation. Your career can benefit.

Once you become institutionalized, the corporate ladder is all you know.

You're bubbled. Extremists term it the corporate Matrix. I'm not so severe because the business world brainwashed me, too.

This boosted my corporate career.

Until I hit bottom.

15 months later, I view my corporate life differently. You may wish to advance professionally. Read this before you do.

Your happiness in the workplace may be deceptive.

I've been fortunate to spend time with corporate aces.

Working for 2.5 years in banking social media gave me some of these experiences. Earlier in my career, I recorded interviews with business leaders.

These people have titles like Chief General Manager and Head Of. New titles brought life-changing salaries.

They seemed happy.

I’d pass them in the hallway and they’d smile or shake my hand. I dreamt of having their life.

The ominous pattern

Unfiltered talks with some of them revealed a different world.

They acted well. They were skilled at smiling and saying the correct things. All had the same dark pattern, though.

Something felt off.

I found my conversations with them were generally for their benefit. They hoped my online antics as a writer/coach would shed light on their dilemma.

They'd tell me they wanted more. When you're one position away from CEO, it's hard not to wonder if this next move will matter.

What really displeased corporate ladder chasers

Before ascending further, consider these.

Zero autonomy

As you rise in a company, your days get busier.

Many people and initiatives need supervision. Everyone expects you to know business details. Weak when you don't. A poor leader is fired during the next restructuring and left to pursue their corporate ambition.

Full calendars leave no time for reflection. You can't have a coffee with a friend or waste a day.

You’re always on call. It’s a roll call kinda life.

Unable to express oneself freely

My 8 years of LinkedIn writing helped me meet these leaders.

I didn't think they'd care. Mistake.

Corporate leaders envied me because they wanted to talk freely again without corporate comms or a PR firm directing them what to say.

They couldn't share their flaws or inspiring experiences.

They wanted to.

Every day they were muzzled eroded by their business dream.

Limited family time

Top leaders had families.

They've climbed the corporate ladder. Nothing excellent happens overnight.

Corporate dreamers rarely saw their families.

Late meetings, customer functions, expos, training, leadership days, team days, town halls, and product demos regularly occurred after work.

Or they had to travel interstate or internationally for work events. They used bags and motel showers.

Initially, they said business class flights and hotels were nice. They'd get bored. 5-star hotels become monotonous.

No hotel beats home.

One leader said he hadn't seen his daughter much. They used to Facetime, but now that he's been gone so long, she rarely wants to talk to him.

So they iPad-parented.

You're miserable without your family.

Held captive by other job titles

Going up the business ladder seems like a battle.

Leaders compete for business gains and corporate advancement.

I saw shocking filthy tricks. Leaders would lie to seem nice.

Captives included top officials.

A different section every week. If they ran technology, the Head of Sales would argue their CRM cost millions. Or an Operations chief would battle a product team over support requests.

After one conflict, another began.

Corporate echelons are antagonistic. Huge pay and bonuses guarantee bad behavior.

Overly centered on revenue

As you rise, revenue becomes more prevalent. Most days, you'd believe revenue was everything. Here’s the problem…

Numbers drain us.

Unless you're a closet math nerd, contemplating and talking about numbers drains your creativity.

Revenue will never substitute impact.

Incapable of taking risks

Corporate success requires taking fewer risks.

Risks can cause dismissal. Risks can interrupt business. Keep things moving so you may keep getting paid your enormous salary and bonus.

Restructuring or layoffs are inevitable. All corporate climbers experience it.

On this fateful day, a small few realize the game they’ve been trapped in and escape. Most return to play for a new company, but it takes time.

Addiction keeps them trapped. You know nothing else. The rest is strange.

You start to think “I’m getting old” or “it’s nearly retirement.” So you settle yet again for the trappings of the corporate ladder game to nowhere.

Should you climb the corporate ladder?

Let me end on a surprising note.

Young people should ascend the corporate ladder. It teaches you business skills and helps support your side gig and (potential) online business.

Don't get trapped, shackled, or muzzled.

Your ideas and creativity become stifled after too much gaming play.

Corporate success won't bring happiness.

Find fulfilling employment that matters. That's it.

Luke Plunkett

4 years ago

Gran Turismo 7 Update Eases Up On The Grind After Fan Outrage

Polyphony Digital has changed the game after apologizing in March.

To make amends for some disastrous downtime, Gran Turismo 7 director Kazunori Yamauchi announced a credits handout and promised to “dramatically change GT7's car economy to help make amends” last month. The first of these has arrived.

The game's 1.11 update includes the following concessions to players frustrated by the economy and its subsequent grind:

-

The last half of the World Circuits events have increased in-game credit rewards.

-

Modified Arcade and Custom Race rewards

-

Clearing all circuit layouts with Gold or Bronze now rewards In-game Credits. Exiting the Sector selection screen with the Exit button will award Credits if an event has already been cleared.

-

Increased Credits Rewards in Lobby and Daily Races

-

Increased the free in-game Credits cap from 20,000,000 to 100,000,000.

Additionally, “The Human Comedy” missions are one-hour endurance races that award “up to 1,200,000” credits per event.

This isn't everything Yamauchi promised last month; he said it would take several patches and updates to fully implement the changes. Here's a list of everything he said would happen, some of which have already happened (like the World Cup rewards and credit cap):

- Increase rewards in the latter half of the World Circuits by roughly 100%.

- Added high rewards for all Gold/Bronze results clearing the Circuit Experience.

- Online Races rewards increase.

- Add 8 new 1-hour Endurance Race events to Missions. So expect higher rewards.

- Increase the non-paid credit limit in player wallets from 20M to 100M.

- Expand the number of Used and Legend cars available at any time.

- With time, we will increase the payout value of limited time rewards.

- New World Circuit events.

- Missions now include 24-hour endurance races.

- Online Time Trials added, with rewards based on the player's time difference from the leader.

- Make cars sellable.

The full list of updates and changes can be found here.

Read the original post.

Ben

3 years ago

The Real Value of Carbon Credit (Climate Coin Investment)

Disclaimer : This is not financial advice for any investment.

TL;DR

You might not have realized it, but as we move toward net zero carbon emissions, the globe is already at war.

According to the Paris Agreement of COP26, 64% of nations have already declared net zero, and the issue of carbon reduction has already become so important for businesses that it affects their ability to survive. Furthermore, the time when carbon emission standards will be defined and controlled on an individual basis is becoming closer.

Since 2017, the market for carbon credits has experienced extraordinary expansion as a result of widespread talks about carbon credits. The carbon credit market is predicted to expand much more once net zero is implemented and carbon emission rules inevitably tighten.

Hello! Ben here from Nonce Classic. Nonce Classic has recently confirmed the tremendous growth potential of the carbon credit market in the midst of a major trend towards the global goal of net zero (carbon emissions caused by humans — carbon reduction by humans = 0 ). Moreover, we too believed that the questions and issues the carbon credit market suffered from the last 30–40yrs could be perfectly answered through crypto technology and that is why we have added a carbon credit crypto project to the Nonce Classic portfolio. There have been many teams out there that have tried to solve environmental problems through crypto but very few that have measurable experience working in the carbon credit scene. Thus we have put in our efforts to find projects that are not crypto projects created for the sake of issuing tokens but projects that pragmatically use crypto technology to combat climate change by solving problems of the current carbon credit market. In that process, we came to hear of Climate Coin, a veritable carbon credit crypto project, and us Nonce Classic as an accelerator, have begun contributing to its growth and invested in its tokens. Starting with this article, we plan to publish a series of articles explaining why the carbon credit market is bullish, why we invested in Climate Coin, and what kind of project Climate Coin is specifically. In this first article let us understand the carbon credit market and look into its growth potential! Let’s begin :)

The Unavoidable Entry of the Net Zero Era

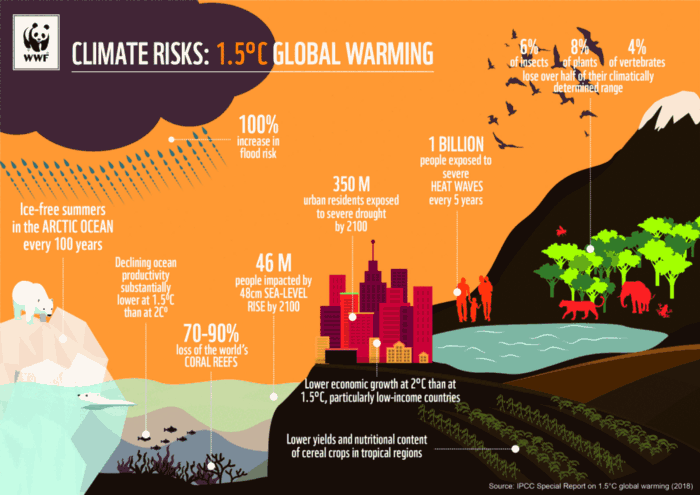

Net zero means... Human carbon emissions are balanced by carbon reduction efforts. A non-environmentalist may find it hard to accept that net zero is attainable by 2050. Global cooperation to save the earth is happening faster than we imagine.

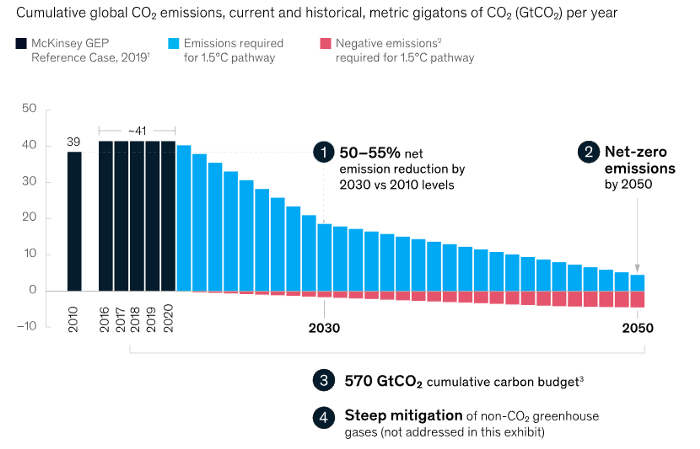

In the Paris Agreement of COP26, concluded in Glasgow, UK on Oct. 31, 2021, nations pledged to reduce worldwide yearly greenhouse gas emissions by more than 50% by 2030 and attain net zero by 2050. Governments throughout the world have pledged net zero at the national level and are holding each other accountable by submitting Nationally Determined Contributions (NDC) every five years to assess implementation. 127 of 198 nations have declared net zero.

Each country's 1.5-degree reduction plans have led to carbon reduction obligations for companies. In places with the strictest environmental regulations, like the EU, companies often face bankruptcy because the cost of buying carbon credits to meet their carbon allowances exceeds their operating profits. In this day and age, minimizing carbon emissions and securing carbon credits are crucial.

Recent SEC actions on climate change may increase companies' concerns about reducing emissions. The SEC required all U.S. stock market companies to disclose their annual greenhouse gas emissions and climate change impact on March 21, 2022. The SEC prepared the proposed regulation through in-depth analysis and stakeholder input since last year. Three out of four SEC members agreed that it should pass without major changes. If the regulation passes, it will affect not only US companies, but also countless companies around the world, directly or indirectly.

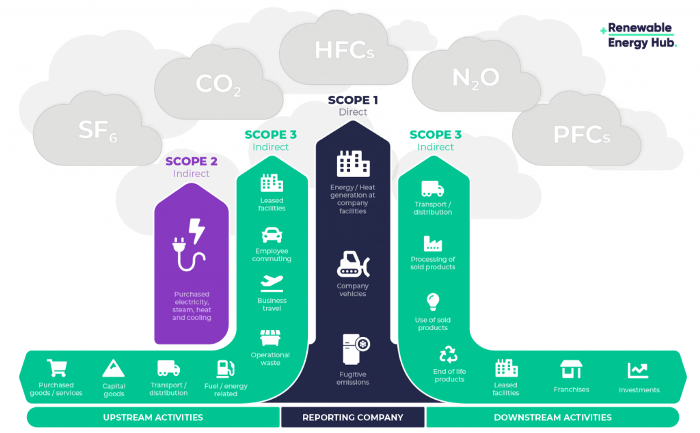

Even companies not listed on the U.S. stock market will be affected and, in most cases, required to disclose emissions. Companies listed on the U.S. stock market with significant greenhouse gas emissions or specific targets are subject to stricter emission standards (Scope 3) and disclosure obligations, which will magnify investigations into all related companies. Greenhouse gas emissions can be calculated three ways. Scope 1 measures carbon emissions from a company's facilities and transportation. Scope 2 measures carbon emissions from energy purchases. Scope 3 covers all indirect emissions from a company's value chains.

The SEC's proposed carbon emission disclosure mandate and regulations are one example of how carbon credit policies can cross borders and affect all parties. As such incidents will continue throughout the implementation of net zero, even companies that are not immediately obligated to disclose their carbon emissions must be prepared to respond to changes in carbon emission laws and policies.

Carbon reduction obligations will soon become individual. Individual consumption has increased dramatically with improved quality of life and convenience, despite national and corporate efforts to reduce carbon emissions. Since consumption is directly related to carbon emissions, increasing consumption increases carbon emissions. Countries around the world have agreed that to achieve net zero, carbon emissions must be reduced on an individual level. Solutions to individual carbon reduction are being actively discussed and studied under the term Personal Carbon Trading (PCT).

PCT is a system that allows individuals to trade carbon emission quotas in the form of carbon credits. Individuals who emit more carbon than their allotment can buy carbon credits from those who emit less. European cities with well-established carbon credit markets are preparing for net zero by conducting early carbon reduction prototype projects. The era of checking product labels for carbon footprints, choosing low-emissions transportation, and worrying about hot shower emissions is closer than we think.

The Market for Carbon Credits Is Expanding Fearfully

Compliance and voluntary carbon markets make up the carbon credit market.

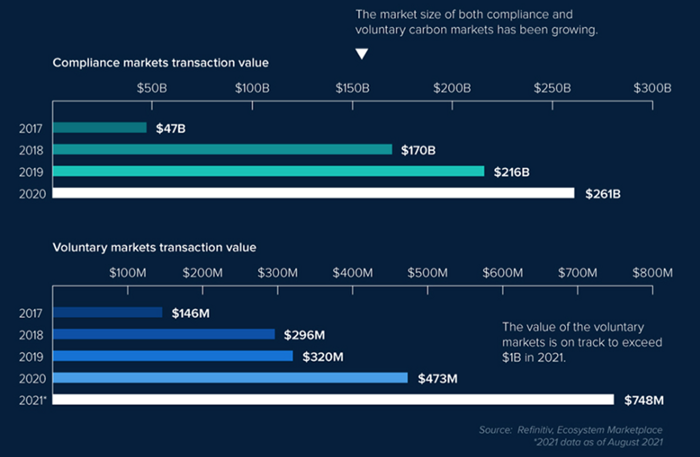

A Compliance Market enforces carbon emission allowances for actors. Companies in industries that previously emitted a lot of carbon are included in the mandatory carbon market, and each government receives carbon credits each year. If a company's emissions are less than the assigned cap and it has extra carbon credits, it can sell them to other companies that have larger emissions and require them (Cap and Trade). The annual number of free emission permits provided to companies is designed to decline, therefore companies' desire for carbon credits will increase. The compliance market's yearly trading volume will exceed $261B in 2020, five times its 2017 level.

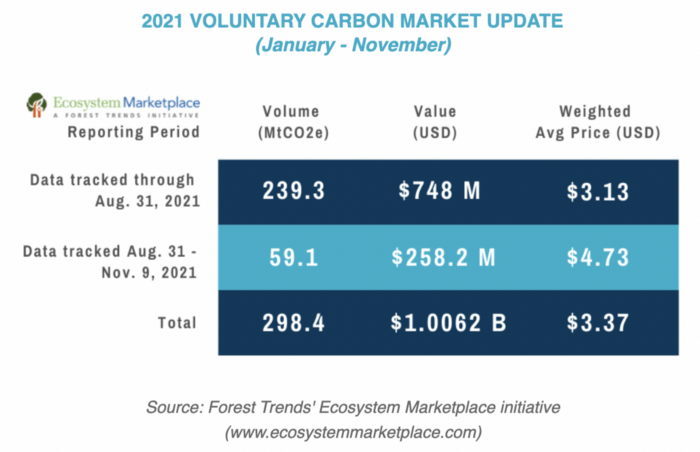

In the Voluntary Market, carbon reduction is voluntary and carbon credits are sold for personal reasons or to build market participants' eco-friendly reputations. Even if not in the compliance market, it is typical for a corporation to be obliged to offset its carbon emissions by acquiring voluntary carbon credits. When a company seeks government or company investment, it may be denied because it is not net zero. If a significant shareholder declares net zero, the companies below it must execute it. As the world moves toward ESG management, becoming an eco-friendly company is no longer a strategic choice to gain a competitive edge, but an important precaution to not fall behind. Due to this eco-friendly trend, the annual market volume of voluntary emission credits will approach $1B by November 2021. The voluntary credit market is anticipated to reach $5B to $50B by 2030. (TSCVM 2021 Report)

In conclusion

This article analyzed how net zero, a target promised by countries around the world to combat climate change, has brought governmental, corporate, and human changes. We discussed how these shifts will become more obvious as we approach net zero, and how the carbon credit market would increase exponentially in response. In the following piece, let's analyze the hurdles impeding the carbon credit market's growth, how the project we invested in tries to tackle these issues, and why we chose Climate Coin. Wait! Jim Skea, co-chair of the IPCC working group, said,

“It’s now or never, if we want to limit global warming to 1.5°C” — Jim Skea

Join nonceClassic’s community:

Telegram: https://t.me/non_stock

Youtube: https://www.youtube.com/channel/UCqeaLwkZbEfsX35xhnLU2VA

Twitter: @nonceclassic

Mail us : general@nonceclassic.org